- Joined

- 13 February 2006

- Posts

- 4,994

- Reactions

- 11,213

So May is (pretty much) in the books now:

The Indices:

All 3 look stretched and ready to roll over.

Top 3

Bottom 3

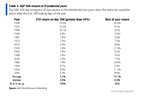

Seasonality

June typically is an up month, but only very marginally: 0.6%.

With everything chartwise looking horrible, I think June could be ugly.

jog on

duc

The Indices:

All 3 look stretched and ready to roll over.

Top 3

Bottom 3

Seasonality

June typically is an up month, but only very marginally: 0.6%.

With everything chartwise looking horrible, I think June could be ugly.

jog on

duc