Timmy

white swans need love too

- Joined

- 30 September 2007

- Posts

- 3,457

- Reactions

- 3

Economists still view the index as a barometer of global productivity trends, but "it appears there are some growing concerns about its usefulness today versus its usefulness, say, two years ago. And it's all down to shipping supply," Izabella Kaminska at FT Alphaville wrote on Wednesday.

Aarbee wrote some really good stuff in post number 27 regarding the peculiarities of the BDI (especially as relates to new ship supply entering the market ... sort of like an increase in open interest!).

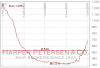

Anyone done any investigation of the HARPEX index? Looks at container-ship rates. Link: http://www.harperpetersen.com/harpex/harpexVP.do

Attached is a description of the HARPEX, pdf format.

https://www.aussiestockforums.com/forums/attachment.php?attachmentid=37834&stc=1&d=1278643096

Would put up a chart but the link not working for me at the moment.

")