You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Baltic Dry Index

- Thread starter Lucky_Country

- Start date

wayneL

VIVA LA LIBERTAD, CARAJO!

- Joined

- 9 July 2004

- Posts

- 26,024

- Reactions

- 13,370

Re: International Index Trading

"If" T/A applies on an index like this, it's broken downwards from that triangle consolidation.

....with $BDI still taking a whopping.important to note for the Aussie market, scrolling down is the relationship between BDI & the CRB index, with BDI clearly leading

"If" T/A applies on an index like this, it's broken downwards from that triangle consolidation.

- Joined

- 17 January 2007

- Posts

- 2,986

- Reactions

- 32

China’s statistics bureau said exports slid 23 percent in July from a year earlier, and the central bank reported that new loans plunged to less than a quarter of June’s level.

Attachments

Timmy

white swans need love too

- Joined

- 30 September 2007

- Posts

- 3,457

- Reactions

- 3

Yep, lots of economic stats out of China yesterday. On balance (gross oversimplification coming up, read articles for fuller picture and DYOR) showing growth but a little below expectations, and lending fell sharply from June.

Reuters: China's economy takes a breather; recovery intact

BBC: China economy shows improvement

Bloomberg: China May Delay Monetary Tightening as Exports, New Loans Drop

Back on topic, BDI should be an indicator for global growth, appears very closely correlated with oil too. Useful part of the picture.

Reuters: China's economy takes a breather; recovery intact

BBC: China economy shows improvement

Bloomberg: China May Delay Monetary Tightening as Exports, New Loans Drop

Back on topic, BDI should be an indicator for global growth, appears very closely correlated with oil too. Useful part of the picture.

- Joined

- 17 January 2007

- Posts

- 2,986

- Reactions

- 32

http://www.spiegel.de/international/business/0,1518,641513,00.htmlThe global economic crisis is wreaking havoc on shipping: Demand and prices have collapsed and ports are filling up with fleets of empty freighters. The crisis has fueled cut-throat competition and not all companies will survive. Germany's Hapag-Lloyd alone needs 1.75 billion euros to stay afloat.

Over the course of the current crisis, investors have had their vocabularies enhanced with terms such as “credit default derivatives,” “quantitative easing,” and the “Baltic Dry Index,” terms that previously were used only by a very small cadre of cognoscenti.

The latter, which takes measure of global shipping activity, is viewed as a quick way to gauge the robustness of global economic health. Logically, as empty ships don’t wander the world like Flying Dutchmen looking for a load, they remain parked when business is bad. On the other hand, if the pistons of global commerce are pumping madly, then so will the engines of the multitude of ships on the Seven Seas.

Today, we‘re assured that the world’s business is on the mend and that all is well. Someone might want to pass that information on to Germany’s Hapag-Lloyd, a 160-year-old shipping firm considered to be one of the world’s most efficient. Unfortunately, even their acknowledged management skills are unable to protect the company from the collapse in shipping prices: it costs about $800 to ship a container from Asia to Europe, but excess capacity in the face of plummeting international commerce has driven the going rate to just $300.

Kinda hard to make up a $500 shortfall per container on volume, eh?

So dire is the situation, according to an excellent article in Spiegel Online, that the company hemorrhaged 220 million euros in the first quarter of this year alone and is headed for an inglorious end of its long and storied history if it can’t come up with $1.7 billion euros pronto.

A snippet from the Spiegel article…How will you know the crisis is really over? Well, for starters, watch shipping rates. Because as long as they remain in Mr. Jones’ proverbial locker, well below the cost of actually shipping the goods, it’s a pretty clear signal that the sailing is anything but clear.

- Leading shipping line operators are on the verge of bankruptcy, as are shipping banks and charter shipping companies. The industry, once one of the biggest beneficiaries of globalization, now threatens to turn into one of its chief casualties.

"There has never been a crisis like this before," says Reinhard Lange, the CEO of Kühne + Nagel, the world's largest sea-freight forwarder. Shipping line operators alone are expected to suffer combined losses of $20 billion in 2009.

Drewry Shipping Consultants, the world's top consultant to the industry, warns: "The industry is looking at the edge of a deep abyss."

- Joined

- 10 July 2004

- Posts

- 2,913

- Reactions

- 3

Leading shipping line operators are on the verge of bankruptcy, as are shipping banks and charter shipping companies. The industry, once one of the biggest beneficiaries of globalization, now threatens to turn into one of its chief casualties.

"There has never been a crisis like this before," says Reinhard Lange, the CEO of Kühne + Nagel, the world's largest sea-freight forwarder. Shipping line operators alone are expected to suffer combined losses of $20 billion in 2009.

Drewry Shipping Consultants, the world's top consultant to the industry, warns: "The industry is looking at the edge of a deep abyss."

Oh. Don't green shoots like sea water?

Oh. Only THOSE green shoots, huh? *Sea WEED*.

Hmmm...

- Joined

- 21 June 2005

- Posts

- 105

- Reactions

- 0

While studying the BDI for clues towards the future of world economy a few things should be considered:

The shipping market is very cyclical. Newer ships get built and the older ones get scrapped and of course, the shipping freight and time-charter rates adjust according to supply and demand. However, due to it's very nature, raising finance, ordering, building of ship's introduces a lag in the supply of ships. Over the last 100 years the same pattern gets repeated time and time again. In boom times, ships are ordered way in excess and that then leads to a bust and the story repeats itself. Greed and Fear I hear you say - of course!!

In the few years before the last bust in 2008, there was a frenzy of shipbuilding. Not just ship's were shipyards were ordered to build more bulk carriers in a hurry. Workers in the major shipbreaking yard like Alang were basically unemployed. Any old junkbucket that could float was pressed into service and attracted good hire rates. Bulk carrier hire rates went up by a 1000 percent. Just when the rate of new vessels from brand new shipyards hitting the water hit an all time high, the GFC came around. It was a perfect storm for dry shipping.

No surprise, the BDI dropped by 94% or thereabouts. Hundreds of ship's on order were cancelled. Shipyards went bankrupt and so did some very big names in the ship chartering community.

Now there is a long waiting time to have your ships scrapped!!!

The anchorages in places like Singapore are choking with ships just lying idle awaiting employment at breakeven rates.

The shorter term movements of the BDI are very susceptible to things like short term policy changes by the Chinese government, the Chinese stockpiles of ore or surge in thermal coal requirements in India. One of the major reasons for BDI spikes in 2007-2008 was the sudden decision by Chinese to raise their stockpiles of iron ore. This by itself would have an effect but what compounded it was the inadequacy of ports infrastructure. There were upto 150 ships waiting long periods of time at Newcastle and Haypoint to load coal and similarly there were large nos of ships waiting at Chinese ports to discharge iron ore. This takes a sizeable chunk of tonnage from active service and puts severe upward pressure on shipping freight and time-charter hire rates.

China has built many new deep ports and we are in the process of building new port infrastructure in Oz albeit, too little, too late and too slowly.

The shipping market is still depressed and who knows what tomorrow holds. Shipping is a derived demand and the dry bulk shipping is a good indicator of the world economy. With more and more old tonnage being scrapped, there would be a balance and the BDI would be that much more accurate in reflecting the actual state of world economy. In the meantime, the short term movements of the BDI should be only seen in the larger context.

Cheers

The shipping market is very cyclical. Newer ships get built and the older ones get scrapped and of course, the shipping freight and time-charter rates adjust according to supply and demand. However, due to it's very nature, raising finance, ordering, building of ship's introduces a lag in the supply of ships. Over the last 100 years the same pattern gets repeated time and time again. In boom times, ships are ordered way in excess and that then leads to a bust and the story repeats itself. Greed and Fear I hear you say - of course!!

In the few years before the last bust in 2008, there was a frenzy of shipbuilding. Not just ship's were shipyards were ordered to build more bulk carriers in a hurry. Workers in the major shipbreaking yard like Alang were basically unemployed. Any old junkbucket that could float was pressed into service and attracted good hire rates. Bulk carrier hire rates went up by a 1000 percent. Just when the rate of new vessels from brand new shipyards hitting the water hit an all time high, the GFC came around. It was a perfect storm for dry shipping.

No surprise, the BDI dropped by 94% or thereabouts. Hundreds of ship's on order were cancelled. Shipyards went bankrupt and so did some very big names in the ship chartering community.

Now there is a long waiting time to have your ships scrapped!!!

The anchorages in places like Singapore are choking with ships just lying idle awaiting employment at breakeven rates.

The shorter term movements of the BDI are very susceptible to things like short term policy changes by the Chinese government, the Chinese stockpiles of ore or surge in thermal coal requirements in India. One of the major reasons for BDI spikes in 2007-2008 was the sudden decision by Chinese to raise their stockpiles of iron ore. This by itself would have an effect but what compounded it was the inadequacy of ports infrastructure. There were upto 150 ships waiting long periods of time at Newcastle and Haypoint to load coal and similarly there were large nos of ships waiting at Chinese ports to discharge iron ore. This takes a sizeable chunk of tonnage from active service and puts severe upward pressure on shipping freight and time-charter hire rates.

China has built many new deep ports and we are in the process of building new port infrastructure in Oz albeit, too little, too late and too slowly.

The shipping market is still depressed and who knows what tomorrow holds. Shipping is a derived demand and the dry bulk shipping is a good indicator of the world economy. With more and more old tonnage being scrapped, there would be a balance and the BDI would be that much more accurate in reflecting the actual state of world economy. In the meantime, the short term movements of the BDI should be only seen in the larger context.

Cheers

- Joined

- 12 September 2004

- Posts

- 1,714

- Reactions

- 1

Excellent summary aarbee.

Just a question if you can provide some idea, but are the "holding costs" (ie the cost of waiting for a ship to be scrapped) exhorbanent? If they are high, surely there is a economical way to put excess shipping to use for bulk storage, scuttled to protect vulnerable coastlines, or some other purpose?

Just a question if you can provide some idea, but are the "holding costs" (ie the cost of waiting for a ship to be scrapped) exhorbanent? If they are high, surely there is a economical way to put excess shipping to use for bulk storage, scuttled to protect vulnerable coastlines, or some other purpose?

- Joined

- 21 June 2005

- Posts

- 105

- Reactions

- 0

Excellent summary aarbee.

Just a question if you can provide some idea, but are the "holding costs" (ie the cost of waiting for a ship to be scrapped) exhorbanent? If they are high, surely there is a economical way to put excess shipping to use for bulk storage, scuttled to protect vulnerable coastlines, or some other purpose?

Well once the shipowner has decided to scrap the ship, it is sold to the buyer at scrap value and delivered to him at the scrapyard. The buyer's loss during waiting is basically the cost of his funds tied up for the duration of waiting period. The ship's machinery etc is salvaged and has some residual value. I don't think the ship can be used for other purposes you outlined especially with unclean bunker tanks.

As for bulk storage, in the very early eighties the oil market had crashed and during the worst period, a lot of tankers were used for storage but there were others including a few brand new tankers which ended being scrapped because even the layup costs were too high. Those were crazy times for the tanker market. The dry bulk market is nowhere close to that situation.

Cheers

Timmy

white swans need love too

- Joined

- 30 September 2007

- Posts

- 3,457

- Reactions

- 3

This is great stuff thanks aarbee.

Timmy

white swans need love too

- Joined

- 30 September 2007

- Posts

- 3,457

- Reactions

- 3

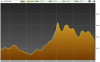

Just updating this thread, chart attached of the BDI. Strongly coming off the late Sept. lows. Sign of confidence in global recovery?

Source of this chart is Stockcharts

http://stockcharts.com/charts/

and more at

http://www.investmenttools.com/futures/bdi_baltic_dry_index.htm

(Thanks for link Edwood)

Source of this chart is Stockcharts

http://stockcharts.com/charts/

and more at

http://www.investmenttools.com/futures/bdi_baltic_dry_index.htm

(Thanks for link Edwood)

Attachments

Lucky_Country

Formerly known as ijh

- Joined

- 30 June 2006

- Posts

- 738

- Reactions

- 0

The BDI chart looking alot healthie lately and with Australian Resources a centrepiece of its activity one must think the good times are not far off.

The US and UK are a drag but slowly improving whereas China is surging ahead and kickstarting the global economey.

The US and UK are a drag but slowly improving whereas China is surging ahead and kickstarting the global economey.

Timmy

white swans need love too

- Joined

- 30 September 2007

- Posts

- 3,457

- Reactions

- 3

wayneL

VIVA LA LIBERTAD, CARAJO!

- Joined

- 9 July 2004

- Posts

- 26,024

- Reactions

- 13,370

- Joined

- 6 January 2009

- Posts

- 2,300

- Reactions

- 1,130

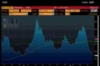

The old triple nipple formation, this is never a good sign.

Cheers

Cheers

Garpal Gumnut

Ross Island Hotel

- Joined

- 2 January 2006

- Posts

- 13,862

- Reactions

- 10,717

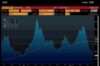

Just keeping us informed on the BDI (weekly chart).

Interesting? Yes? No?

Very very interesting, thanks.

gg

- Joined

- 28 October 2008

- Posts

- 8,609

- Reactions

- 39

It's now at its lowest level in 14 months.

- Joined

- 3 January 2007

- Posts

- 940

- Reactions

- 2

http://www.zerohedge.com/article/ba...secutive-loss-6-years-refutes-australian-opti

So much for the trade surplus recently reported eh?

This is why I am betting on the AUD to fall further. With the Chinese mills are now reporting to be destocking steel inventories and lowering production, how much more "lucky" can this country gets?

I'm always surprised at how uninformed most people are in regards to the recent massive over stockpiling of resources by the Chinese has on the Australian economy. They haven't heard stories about pig farmers speculating on copper prices by stock pilling them in their own warehouses?

Baltic Dry Index Dropping 4%, Posting Longest Consecutive Loss In 6 Years, Refutes Australian Optimism

Submitted by Tyler Durden on 07/06/2010 08:43 -0500

Baltic Dry Real estate

The biggest reason for the runup in the JPYAUD and its immediate secondary carry derivative, the stock market, was the earlier announcement out of the RBA claiming all is clear, there is no bubble in China, there is no bubble in OZ real estate, and all the other usual talking points one would expect out of a central bank whose future is inextricably linked to the endless commodity stocking in China. And indeed, one glance at the far more neutral indicator of the Baltic Dry index paints a far more dire picture: the BDIY plunged 4% overnight to 2,127, posting the longest consecutive decline in 6 years at 28 days. Despite the optimism from the conflicted money printers, those whose livelihood actually depends on a ceaseless influx of goods into China and broader commodity trading in general, are not nearly quite so happy, having seen a drop in their margins by almost 50% in just over a month.

So much for the trade surplus recently reported eh?

This is why I am betting on the AUD to fall further. With the Chinese mills are now reporting to be destocking steel inventories and lowering production, how much more "lucky" can this country gets?

I'm always surprised at how uninformed most people are in regards to the recent massive over stockpiling of resources by the Chinese has on the Australian economy. They haven't heard stories about pig farmers speculating on copper prices by stock pilling them in their own warehouses?

Attachments

nulla nulla

Positive Expectancy

- Joined

- 24 September 2008

- Posts

- 3,588

- Reactions

- 133

The old triple nipple formation, this is never a good sign.

Cheers

could be worse.

- Joined

- 23 March 2005

- Posts

- 1,943

- Reactions

- 1

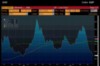

You'd never know that a key marine freight index was plunging by looking at Asian shipping shares' year-to-date performances, and some analysts remain upbeat on freight rates in the long term.

Most Asian shipping shares extended their gains Thursday, as broader markets rallied in the wake of a strong advance on Wall Street.

But the Baltic Dry Index, which tracks sea freight rates to ship dry commodities, fell for the 30th straight day through Wednesday to its lowest level since May 2009. According to the Baltic Exchange, which compiles the index, the BDI fell 5.1% to 2,018 points --down to less than half of its May 26 peak of 4,209.

"It is the longest decline in six years," said Marc Chandler, global head of currency strategy at Brown Brothers Harriman. "The main driver seems to be concerns about the cooling of China's steel sector. Steel is the biggest user of iron ore. Iron ore and coking coal account for more than a third of the Baltic dry freight."

Economists still view the index as a barometer of global productivity trends, but "it appears there are some growing concerns about its usefulness today versus its usefulness, say, two years ago. And it's all down to shipping supply," Izabella Kaminska at FT Alphaville wrote on Wednesday.

TAL International is seen as attractively valued and leveraged to a recovery.

Freight rates could remain low in the third quarter, "as steel mills shut for maintenance, grain shipping ends and concerns over China's falling import demand looms," said J.P Morgan shipping analyst Corrine Png in a research report this week.

"However, we do not expect freight rates to collapse to distress levels [seen] in late 2008, which was exacerbated by trade-finance issues," she said. "The container shipping experience in the past 1.5 years has taught us that pricing at marginal cost is unsustainable, as vessels start getting laid up before long."

As the industry continues to take delivery of new vessels, "this will lend support to longer-term freight rates," she said.

http://www.marketwatch.com/story/asia-shipping-shares-belie-baltic-dry-index-drop-2010-07-07

Most Asian shipping shares extended their gains Thursday, as broader markets rallied in the wake of a strong advance on Wall Street.

But the Baltic Dry Index, which tracks sea freight rates to ship dry commodities, fell for the 30th straight day through Wednesday to its lowest level since May 2009. According to the Baltic Exchange, which compiles the index, the BDI fell 5.1% to 2,018 points --down to less than half of its May 26 peak of 4,209.

"It is the longest decline in six years," said Marc Chandler, global head of currency strategy at Brown Brothers Harriman. "The main driver seems to be concerns about the cooling of China's steel sector. Steel is the biggest user of iron ore. Iron ore and coking coal account for more than a third of the Baltic dry freight."

Economists still view the index as a barometer of global productivity trends, but "it appears there are some growing concerns about its usefulness today versus its usefulness, say, two years ago. And it's all down to shipping supply," Izabella Kaminska at FT Alphaville wrote on Wednesday.

TAL International is seen as attractively valued and leveraged to a recovery.

Freight rates could remain low in the third quarter, "as steel mills shut for maintenance, grain shipping ends and concerns over China's falling import demand looms," said J.P Morgan shipping analyst Corrine Png in a research report this week.

"However, we do not expect freight rates to collapse to distress levels [seen] in late 2008, which was exacerbated by trade-finance issues," she said. "The container shipping experience in the past 1.5 years has taught us that pricing at marginal cost is unsustainable, as vessels start getting laid up before long."

As the industry continues to take delivery of new vessels, "this will lend support to longer-term freight rates," she said.

http://www.marketwatch.com/story/asia-shipping-shares-belie-baltic-dry-index-drop-2010-07-07

Similar threads

- Replies

- 372

- Views

- 26K

- Replies

- 75

- Views

- 11K