CanOz

Home runs feel good, but base hits pay bills!

- Joined

- 11 July 2006

- Posts

- 11,543

- Reactions

- 519

Could be interesting for those who like their yield income.

am I wrong to think the hang seng is offering the best yield / risk play?

http://www.bespokeinvest.com/thinkbig/2014/7/15/country-dividend-yields.html

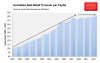

This is a great chart Syd, can you re-post in the International Markets thread? Also can you give the source and / post the update every a Qtr?