DeepState

Multi-Strategy, Quant and Fundamental

- Joined

- 30 March 2014

- Posts

- 1,615

- Reactions

- 81

Which of these central banks.....

Looks most like Varuca Salt?

Looks most like Varuca Salt?

Puts into perspective why the money is still flowing to aussie debt markets.

So Goldman Sachs finds that its Sigma-X dark pool was not actually delivering the best prices to pool participants. FINRA finds that Goldman did not have the proper processes in place from Dec 2008 to Aug 2011. There were 395k transactions between 29 July 2008 to 9 August 2008 alone which contravened the law.

US regulators are filing a suit for $800,000. No, there are no missing zeros at the end of that figure. In addition, Goldman will pay $1.67m (again, that's an 'm' as opposed to 'bn') in restitutions to clients.

This week, BNP Paribas has been fined $9bn for violating sanctions.

Which of these is just? Is the other unjust? Or are they both screwed up?

Data from Bank of America show that oil and gas investment in the US has soared to $200bn a year. It has reached 20pc of total US private fixed investment, the same share as home building. This has never happened before in US history, even during the Second World War when oil production was a strategic imperative.

The real, unanswered question is at what price point the economy "breaks" sufficiently to preclude further growth in total expenditure on oil? That's the real question and a very relevant one on a stocks / investment forum. My guess personally is that the limit is somewhere in the $150 - $200 per barrel range.

Could be interesting for those who like their yield income.

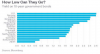

am I wrong to think the hang seng is offering the best yield / risk play?

http://www.bespokeinvest.com/thinkbig/2014/7/15/country-dividend-yields.html

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.