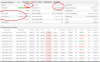

One of the trading records has 360 closed trades and the other has 88 closed trades - not enough trades to be deemed statistically significant (are there any records with +1000 closed trades?).

These are good examples of short term excursions into the "black zone".

The records depict high trade frequencies (+1000 closed trades should be achievable in a couple of months, unless the operator bails on the system - as usual) - please provide links to the records and we can monitor the outcome at +1000 closed trades (if achieved).

Everything is public on myfxbook. Nothing's gonna convince ya, next will be "it's scalping - I'm gonna need to see 30+ years at least to see it holds up". Stay in your bubble, I'm done on this stupid topic of no 50%+&1:1+ in existence.