Havent worked it out have you!

Explain it to me, I'm curious as to how rising interest rates have a positive impact on housing prices.

Havent worked it out have you!

Explain it to me, I'm curious as to how rising interest rates have a positive impact on housing prices.

Havent worked it out have you!

Cost of construction rises as costs----normally wages are passed on---.

If Interest really rockets to curb inflation then its even worse for the non home owner as his money's buying power is eroded.

History has shown many times that economic bubbles pop rather than slowly deflate.

Australia is not immune to this.

Wages haven't increased enough to curb the cost of housing increases.

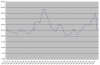

Actually they have - see these charts. One show the median house price to average household disposable income ratio - as you can see that has remained nearly constant for the past 8 years. The other chart plots the proportion of household income required to service the average mortgage since the 70s.

I don't know of too many people getting paid double what they did 10 years ago thoughso why did 4 of your mates sell their houses, were they upgrading, cashing in and going out to rent, leaving the country

Actually they have - see these charts. One show the median house price to average household disposable income ratio - as you can see that has remained nearly constant for the past 8 years. The other chart plots the proportion of household income required to service the average mortgage since the 70s.

Great! Another chart from that unbiased think tank RPData

I wonder where they get their figures from.

The other chart plots the proportion of household income required to service the average mortgage since the 70s.

The number of Australia home loans approved for investment purposes jumped to 34.1% of all mortgages in February, up from 27.1 per cent in August and the highest level of investor interest in the four-year history of the AFG mortgage index.

This has baffled the many analysts who have cautioned that the Australian property market is experiencing the formation of a bubble. It is even more worrying when looked at against the fact that loans to first time buyers fell from 20.9% to 11.3% during the same 6 month period.

Wages don't rise as fast as property prices. I get the argument for inflation leading to rising costs and therefore property prices, I think its artificial unsustainable growth however and doesn't flow down to Mum and Dad or Joe Blow down the street.

Wages haven't increased enough to curb the cost of housing increases. If you argue the point that property doubles every 7-10 years whatever, that's great. So does the guys house who lives next door to you. You don't actually gain any value over and above anyone else.

The way I see it, the Govt gave a whole bunch of people a leg up onto the property ladder who couldn't really afford it. That in turn gave everyone else a push up to the next rung of the ladder. All or the large majority of it is funded by debt.

Everyone of my properties are funded by debt and I get all the interest back as a tax deduction.

again.Cost of construction rises as costs----normally wages are passed on---.

I guarantee it wont!

You said it yourself - there will be fewer sales.

So in turn you'll have more builders competing for fewer jobs. When there is more competition in any field, prices drop to gain your business.

Fewer worker will be hired/more workers will be fired due to the lesser workload and ultimately you'll have cheaper houses.

.

BTW, most of the price of property comes from the land value

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.