nulla nulla

Positive Expectancy

- Joined

- 24 September 2008

- Posts

- 3,588

- Reactions

- 133

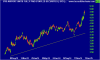

Macquarie block traded the residual stake in SYD which they are not distributing in specie this morning. Stocks usually underperform on the day of a block trade.

Todays papers indicate that Macquarie Bank will distribute its' entire holding in Sydney Airport to the Macquarie Bank share holders on the basis of one Sydney Airport share for every Macquarie Bank share held.

The release from Sydney Airport yesterday welcomed the move noting that this would mean an influx of a large number of small share holders to the share registry (you'd have to wonder if that was tongue in cheek). I suspect that some foreign investors in Macquarie Bank may have to unload their SYD holding to keep SYD inside the contraints of foreign ownership limitations. I also suspect suggestions that this could make SYD a takeover opportunity are a furphy due to the presence of foreign investors and those same limitations.

No doubt the influx of small share holders to the registry will also contribute to some future volitility as they work out whether they want to hold, sell or add to their holdings.

Probably a clever move Macquarie Bank. The original issue price was $2.00, however they have had several capital returns over the years and would likely be looking at a significant capital gains tax if they sold at the present share price $4.07. I would not be surprised if they have obtained a tax ruling that the capital gains will be the responsibility of their share holders at such time as the share holders sell the Sydney Airport shares received.

Then again I could be completely wrong (I don't hold Macquarie Bank shares). As always do your own research and good luck.

")