- Joined

- 8 April 2008

- Posts

- 871

- Reactions

- 0

Good to see NCM directors buying more of their own shares.

Vince Gauci bought 6000 shares at $14.74

Greg Robinson bought 8000 shares at $14.51

Calling CanOz & TechA if I may??!!

Fellas, would be very interested to get your TA on NCM.

I don't see it "unreasonable" for this one to head all the way back to the $6-8 region (worst case scenario) in the next few months.

Looking back on the weekly stretching back 25 years it appears as though this was the start of the huge run up.

I pretty much never buy shares but have been watching this like a hawk and should it reach these levels it will be a screaming buy.

Interested to hear your thoughts, if any?

So a return to low levels 25 yrs ago is your buy criteria?

Calling CanOz & TechA if I may??!!

Fellas, would be very interested to get your TA on NCM.

I don't see it "unreasonable" for this one to head all the way back to the $6-8 region (worst case scenario) in the next few months.

Looking back on the weekly stretching back 25 years it appears as though this was the start of the huge run up.

I pretty much never buy shares but have been watching this like a hawk and should it reach these levels it will be a screaming buy.

Interested to hear your thoughts, if any?

If NCM dropped to $6-8 region it would be a double screaming buy and I think you would have to be lighting quick to buy shares at that price before it bounced up like a super ball.

25 years ago Newcrest was primarily an explorer but with a little bit of production (and it was called Newmont Australia. Only became Newcrest in 1990 after merging with BHP Gold) .Today it is a major gold producing company.

The most recent occassion when the share price was ~$6 was in 2003. At that time Newcrest was producing around 700,000 oz gold and 60,000 tonnes copper per year . Today it produces around 2 million oz gold and 76,000 tonnes copper year. Its gold resources and reserves have each approximatley tripled since 2003 and its copper resources and reserves have increased five-fold.

Newcrest has recently been in an expansion phase which is coming to an end after which production will gradually ramp up to over 3 million oz gold per year.

Profit in 2003 was $168/oz gold produced. In 2012 profit was $493/oz gold produced.

I will not bother going into other financials except that at the current share price NCM is already below book value.

Newcrest is already a screaming buy at around $14.50. Market sentiment and languishing gold price might still send it down a bit more but the downside risk is far smaller IMO than the upside potential.

Disclosure: I am accumulating NCM aggressively at current prices.

I see.

What would the price of gold have to get to for profit to revert back to or below the $168/oz mark as was the case in 2003?

Have production costs increased or decreased since then?

I can give you an opinion on your POG threshold question but not immediately as I don't have access to my cashflow models at the moment.

Production costs have increased and sustaining capex has increased but so has profitability. The question to ask is, given current and projected profitability what is a fair value for the share price? I have my personal opinion on this which is the basis of my investment decision in NCM and I invest for the long term. I am not a 'trader'.

If you are interested I will PM you later this evening. But I cannot give you advice. I can only state my opinions.

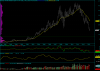

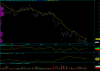

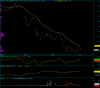

FWIW the auction is still one timing lower with no access low on the monthly's or the weekly's yet, but there is some bracketing on the current daily lows but yet no access low.

CanOz

Thanks CanOZ!

So what indicator will help you determine the access low?

Is a huge volume spike plus long tail sufficient?

Thanks.

Only became Newcrest in 1990 after merging with BHP Gold) .Today it is a major gold producing company.

I'm calling a crack of support and blood on the streets. Gold is down 0.5% from Aus close, if the US fails to inspire we can see lots of stop loss selling tomorrow.

View attachment 52642

Does this have an ADR somewhere? I seem to recall it does....

US: NCMGY

Volume is mediocre

Also trades as NM in Canada but volume there is virtually nonexistant

I'm sure you realise - but today there are 766m shares on issue. In the middle of 2003 there were about 326m. A share price of $6 in today's terms would have a much higher EV than in 2003. I always tread with caution when dealing in historical share prices, because they are often not as equivalent as they seem.The most recent occassion when the share price was ~$6 was in 2003.

I'm sure you realise - but today there are 766m shares on issue. In the middle of 2003 there were about 326m. A share price of $6 in today's terms would have a much higher EV than in 2003. I always tread with caution when dealing in historical share prices, because they are often not as equivalent as they seem.

Probably irrelevant to your discussion perhaps.... but I thought someone might find it useful.

I'm sure you realise - but today there are 766m shares on issue. In the middle of 2003 there were about 326m. A share price of $6 in today's terms would have a much higher EV than in 2003. I always tread with caution when dealing in historical share prices, because they are often not as equivalent as they seem.

Probably irrelevant to your discussion perhaps.... but I thought someone might find it useful.

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.

")