- Joined

- 16 June 2008

- Posts

- 147

- Reactions

- 0

Re: MAH - Up or Down

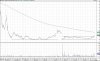

Hello,

Not much comment here on MAH since March so assume not very many interested at ASF.

Need some assistance in reading recent chart seems to get support up to $1.70 then falls back slightly. If you look at course of sales last week or so lots of very small trades some smartie buys 25 then sells 25 about 30 mins later.

Hope one of you chartist can have look and give your opinion , is it going to break the $1.70 or fall away.

Regards

Hello,

Not much comment here on MAH since March so assume not very many interested at ASF.

Need some assistance in reading recent chart seems to get support up to $1.70 then falls back slightly. If you look at course of sales last week or so lots of very small trades some smartie buys 25 then sells 25 about 30 mins later.

Hope one of you chartist can have look and give your opinion , is it going to break the $1.70 or fall away.

Regards

![chart[1].gif](https://aussiestockforums.b-cdn.net/data/attachments/20/20001-3aab7fe8d16207d459e6fcd0868c49e3.jpg)