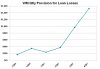

How low can US Housing go?

NEW RESIDENTIAL SALES IN NOVEMBER 2007

Sales of new one-family houses in November 2007 were at a seasonally adjusted annual rate of 647,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 9.0 percent ( ±13.9%)* below the revised October rate of 711,000 and is 34.4 percent ( ±7.9%) below the November 2006 estimate of 987,000.

The median sales price of new houses sold in November 2007 was $239,100; the average sales price was $293,300. The seasonally adjusted estimate of new houses for sale at the end of November was 505,000. This represents a supply of 9.3 months at the current sales rate.