Kauri

E/W Learner

- Joined

- 3 September 2005

- Posts

- 3,428

- Reactions

- 11

Can't believe no one has posted about rio's take over of alcan yet. Would love to know peoples thoughts, seem to have paid a hefty premium over the share price. Some 60 percent over all time highs. Would people think this will move the share price up, or have they paid to much of a premium even though alcan have a supposed quality portfolio?

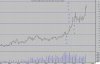

I was looking at some support and resistance points for RIO going back over the past 10 years and noted an amazing pattern of support and resistance points at $23 intervals. The next "$23" resistance point is $111.

I'm not given to predictions and am no Yogi. I am however smarter than the average bear, and would be interested should RIO retrace from $111 back down to $88 which was the last previous resistance.

Enclosed is the monthly chart of RIO back to 1997

Garpal

Morningstar - http://www.investordaily.com.au/stockoftheweek.htm

Stock of the week

Current

Rio Tinto Limited (RIO)

Upgrade of Commodity Price Forecasts

Ongoing growth in Chinese metals consumption followed by India, mining industry input cost inflation, industry consolidation, infrastructure bottlenecks, a scarcity of quality resources due to years of exploration neglect and sovereign risk are all underpinning commodity price strength. The long run average marginal cost of production has jumped permanently higher for most commodities. Much of the new demand has been satisfied by substantially higher cost mines. Australia is a major beneficiary of the macro economic fundamentals and not surprising our currency continues to rise, at last count 86.8 US cents versus our long term forecast of 0.76. We have previously been in no great hurry to increase that long term number as our commodity price forecasts are cast with an eye more firmly on the A$ prices, rather than US dollar prices. The ratio of the A$/US$ exchange rate versus US dollar commodity prices is more important. We now upgrade our long term A$/US$ exchange rate outlook to 0.80. We also upgrade commodity prices and then some! Our commodity price upgrades show the exposure to iron ore and aluminium to a lesser extent. Rio is the class act in iron ore, by a whisker from BHP. The acquisition of Alcan may well prove a masterstroke. A nice free option on an energy and carbon constrained world, without the hassles of construction delays and cost blow outs that come with building capacity.

Alcan joins Rio Tinto to create global aluminium leader

Alcan today joined the Rio Tinto group following the successful Offer for Alcan by a subsidiary of Rio Tinto. The expanded aluminium product group, formed by the combination of Alcan and Rio Tinto's existing aluminium assets, today became the new global leader in aluminium and will be known as Rio Tinto Alcan.

Rio Tinto chief executive, Tom Albanese and Rio Tinto Alcan chief executive, Dick Evans hosted special events at Rio Tinto Alcan's Montreal headquarters and highlighted the opportunities created by bringing Alcan into the Rio Tinto Group, and the potential for continued strong growth in the aluminium sector. Similar employee events took place in Brisbane.

It has begun!

Rio Tinto has stepped up to the next level in the commodities fight, I hope everyone who holds Rio is excited as I am about the Alcan acquisition.

Last I checked analysts at Morningstar & I think UBS and several others rated it $122+, but I think it could go much much higher given aluminum's potential.

Agencies are just jumping on a bandwagon and downgrading most big deals because of the sub-prime collapse.

Judge Rio & Alcan merge for yourself, it soared $6 today, they can keep downgrading howmuchever they want, these are 2 of the best managed businesses out there.

Yeah but note that CommSec has not published Rio's 2010 forecast, and Rio is the first one to have dropped its profit while BHP has maintained substantial rises.

Anyway those numbers could substantially appreciate should demand keep at current levels and US housing reverse past 2009.

The valuations are fair, even the world's biggest company (Mobil) has a valuation of 13, and China/India demand is huge.Hey guys.......just a valuation question, are you guys happy to pay 14 X 2010 earnings for mining companies.......it just seems like things are getting a little out of hand......these aren't growth companies, they are cyclicals who just dig stuff out of the ground and sell it......unless these are last available deposits of these resources on earth making these guys an 'asset play', one would have to have grave doubts about these valuations.....just wouldn't mind discussion is all

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.

...

...