You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

MQG vs. BNB - which is best?

- Thread starter JeffB

- Start date

-

- Tags

- bnb mqg which is best

- Joined

- 1 September 2005

- Posts

- 119

- Reactions

- 0

Re: MBL vs BNB- which is best?

ABN AMRO Broker Up Grade for both stocks

FYI - Rationale

MBL & BNB – Time to Buy back in …

Our analysis shows that the downside risks to valuations for MBL and BNB are limited. Given strong business models, we believe that in the near term both stocks will continue to be bolstered by upgrades. We move both stocks from Add to Buy.

Sensitivity testing for key risks shows limited downside...

The key risks to our valuations and target prices for Macquarie Bank (MBL) and Babcock & Brown (BNB) are a downturn in equity markets, a rise in interest rates and an increase in competition. Our sensitivity testing of all three events shows a surprising resilience by both banks to negative shocks over the next 12-18 months, with the maximum valuation impact resulting from a rise in interest rates, decreasing valuations for MBL by 12% and for BNB by 22%.

...and both banks now well positioned for the medium term

In our view, there are important counter-arguments to concerns about the risks mentioned above. Firstly, both banks have raised enough equity over the past 12 months to continue with rapid asset growth even in a market downturn. Secondly, international diversification provides the opportunity to search for assets and capital on a global scale. Thirdly, the increasing brand recognition of both firms provides them with a distinct competitive advantage compared with any newcomers.

Biggest issue is keeping the fee pipeline full

Given the level of spare capacity at both MBL and BNB, we believe the main impediment to their growth in the near to medium term will be finding suitable assets in which to invest while maintaining a disciplined approach to acquisitions. Longer term, MBL and BNB will need to raise further capital to support the continued rollout of their specialised funds and, as such, are vulnerable to future market conditions.

Upgrades to earnings forecasts, price targets and recommendations

In the near term, we believe MBL and BNB's share prices will continue to be bolstered by earnings upgrades. Accordingly, we lift our forecasts for the next couple of years by about 5% for both stocks. Further out, reduced visibility leads us to a more cautious approach. Nevertheless, with the rise in our price target for MBL from A$80.85 to A$84.72 and the retention of our A$20.00 price target for BNB, there is now more than 20% upside potential to our targets for both stocks. Hence, we raise our recommendations on both from Add to Buy.

ABN AMRO Broker Up Grade for both stocks

FYI - Rationale

MBL & BNB – Time to Buy back in …

Our analysis shows that the downside risks to valuations for MBL and BNB are limited. Given strong business models, we believe that in the near term both stocks will continue to be bolstered by upgrades. We move both stocks from Add to Buy.

Sensitivity testing for key risks shows limited downside...

The key risks to our valuations and target prices for Macquarie Bank (MBL) and Babcock & Brown (BNB) are a downturn in equity markets, a rise in interest rates and an increase in competition. Our sensitivity testing of all three events shows a surprising resilience by both banks to negative shocks over the next 12-18 months, with the maximum valuation impact resulting from a rise in interest rates, decreasing valuations for MBL by 12% and for BNB by 22%.

...and both banks now well positioned for the medium term

In our view, there are important counter-arguments to concerns about the risks mentioned above. Firstly, both banks have raised enough equity over the past 12 months to continue with rapid asset growth even in a market downturn. Secondly, international diversification provides the opportunity to search for assets and capital on a global scale. Thirdly, the increasing brand recognition of both firms provides them with a distinct competitive advantage compared with any newcomers.

Biggest issue is keeping the fee pipeline full

Given the level of spare capacity at both MBL and BNB, we believe the main impediment to their growth in the near to medium term will be finding suitable assets in which to invest while maintaining a disciplined approach to acquisitions. Longer term, MBL and BNB will need to raise further capital to support the continued rollout of their specialised funds and, as such, are vulnerable to future market conditions.

Upgrades to earnings forecasts, price targets and recommendations

In the near term, we believe MBL and BNB's share prices will continue to be bolstered by earnings upgrades. Accordingly, we lift our forecasts for the next couple of years by about 5% for both stocks. Further out, reduced visibility leads us to a more cautious approach. Nevertheless, with the rise in our price target for MBL from A$80.85 to A$84.72 and the retention of our A$20.00 price target for BNB, there is now more than 20% upside potential to our targets for both stocks. Hence, we raise our recommendations on both from Add to Buy.

RichKid

PlanYourTrade > TradeYourPlan

- Joined

- 18 June 2004

- Posts

- 3,031

- Reactions

- 5

Re: MBL vs BNB- which is best?

I've changed the title of this thread as there are existing threads on each stock.

So this'll basically be a thread on which one has better prospects and why- basically a comparison.

If comments are stock specific then they can go in the respective thread for MBL or BNB.

I've changed the title of this thread as there are existing threads on each stock.

So this'll basically be a thread on which one has better prospects and why- basically a comparison.

If comments are stock specific then they can go in the respective thread for MBL or BNB.

Re: MBL vs BNB- which is best?

does anyone remember in a recent AFR article, a broking company believes that MBL has price target of about $142 to $146? didn't say time frame. anyone care to comment on that?

BNB... don't they have a group of rich jews behind them? if these jews are supporting BNB, BNB can't go too wrong.

does anyone remember in a recent AFR article, a broking company believes that MBL has price target of about $142 to $146? didn't say time frame. anyone care to comment on that?

BNB... don't they have a group of rich jews behind them? if these jews are supporting BNB, BNB can't go too wrong.

michael_selway

Coal & Phosphate, thats it!

- Joined

- 20 October 2005

- Posts

- 2,397

- Reactions

- 2

Re: MBL vs BNB- which is best?

thx are those 84.72 & 20.00 price targets for the next 12 months from the date of article being written? thanks

Yippyio said:ABN AMRO Broker Up Grade for both stocks

FYI - Rationale

MBL & BNB – Time to Buy back in …

Our analysis shows that the downside risks to valuations for MBL and BNB are limited. Given strong business models, we believe that in the near term both stocks will continue to be bolstered by upgrades. We move both stocks from Add to Buy.

Sensitivity testing for key risks shows limited downside...

The key risks to our valuations and target prices for Macquarie Bank (MBL) and Babcock & Brown (BNB) are a downturn in equity markets, a rise in interest rates and an increase in competition. Our sensitivity testing of all three events shows a surprising resilience by both banks to negative shocks over the next 12-18 months, with the maximum valuation impact resulting from a rise in interest rates, decreasing valuations for MBL by 12% and for BNB by 22%.

...and both banks now well positioned for the medium term

In our view, there are important counter-arguments to concerns about the risks mentioned above. Firstly, both banks have raised enough equity over the past 12 months to continue with rapid asset growth even in a market downturn. Secondly, international diversification provides the opportunity to search for assets and capital on a global scale. Thirdly, the increasing brand recognition of both firms provides them with a distinct competitive advantage compared with any newcomers.

Biggest issue is keeping the fee pipeline full

Given the level of spare capacity at both MBL and BNB, we believe the main impediment to their growth in the near to medium term will be finding suitable assets in which to invest while maintaining a disciplined approach to acquisitions. Longer term, MBL and BNB will need to raise further capital to support the continued rollout of their specialised funds and, as such, are vulnerable to future market conditions.

Upgrades to earnings forecasts, price targets and recommendations

In the near term, we believe MBL and BNB's share prices will continue to be bolstered by earnings upgrades. Accordingly, we lift our forecasts for the next couple of years by about 5% for both stocks. Further out, reduced visibility leads us to a more cautious approach. Nevertheless, with the rise in our price target for MBL from A$80.85 to A$84.72 and the retention of our A$20.00 price target for BNB, there is now more than 20% upside potential to our targets for both stocks. Hence, we raise our recommendations on both from Add to Buy.

thx are those 84.72 & 20.00 price targets for the next 12 months from the date of article being written? thanks

- Joined

- 21 April 2005

- Posts

- 3,922

- Reactions

- 5

Re: MBL vs BNB- which is best?

They are both stuck in quicksand today!

They are both stuck in quicksand today!

RichKid

PlanYourTrade > TradeYourPlan

- Joined

- 18 June 2004

- Posts

- 3,031

- Reactions

- 5

Re: MBL vs BNB- which is best?

Sell vol seems to have reduced a bit for MBL but BNB has had selling pick up a bit in the last few days.

Snake Pliskin said:They are both stuck in quicksand today!

Sell vol seems to have reduced a bit for MBL but BNB has had selling pick up a bit in the last few days.

Re: MBL vs BNB- which is best?

Which is best - your own answer to this question may come down simply to your risk/reward appetite. Some thoughts I had follow- bear in mind my comments are speculative in nature, and you must make your own investment choice. None of us have crystal balls, otherwise I would be in Monte Carlo right now with all the other millionaires...

Both shares are growth shares, with BNB yet to clarify its P/E a bit more (hopefully this December 2005 full year result). Both have had a number of earnings upgrades, with BNB expected to produce a circa $216 million full year profit, following two 20% upgrades. The prospectus forecasted

$154.7 million. BNB's P/E appears to be a little more expensive than MBL's following the respective guidances, but both companies have said their guidances would be "at least" the forecasts made. BNB, with its GPT joint venture or potentially other initiatives, could potentially pull even more income out of the bag, making its P/E look better again. Both companies have been very busy doing further deals globally this year, which are longer term deals, to snowball in the context of future earnings.

Both have been said to deserve the same P/E valuation on the basis that BNB's better growth prospects offset its higher balance sheet risk. On the upside, you could argue BNB has a lot more growth potential, by looking at its trading performance thus far, over and above MBL, which trades on a lower P/E.

Bar the shouting, both these growth shares should do well in buoyant market conditions. Indeed, their very business models are interrelated to the health of the global/Australian economy/markets.

As MBL does well, BNB seems to do even better, to show what it can become. BNB also appears to be even more internationally focussed, which is the next major frontier for MBL's continued growth outside its home market.

In a downturn, the recent October 2005 crunch showed how resilient each share may be in inevitably tougher times. BNB was hurt more than MBL, but did rebound better from its $15 low (helped by the fact it fell more). MBL is better diversified in its operations, while BNB is more specialised and following a mini-mac model.

Both have strong and growing long-term cash flows from global, market-leading assets, to buffer bad times. Such cash flows ensure debt levels are manageable, as do efforts to fix debt interest rates to counter future increases.

MBL's tilt at the LSE and other growing global moves represent the company's next major growth watershed, and should be expected to underpin the continued march of its share price. Of course, what is to stop BNB doing this, or should I say, continuing to follow a similar sounding strategy? BNB may well just be in "catch up", then "pass by" mode. For the present, BNB requires a greater risk appetite in tougher markets, to go with the benefits of its to-date greater finesse during good markets.

-----------------------------------------------------------------------

These are just my own thoughts, not recommendations to you. I am not qualified to give investment advice!

Which is best - your own answer to this question may come down simply to your risk/reward appetite. Some thoughts I had follow- bear in mind my comments are speculative in nature, and you must make your own investment choice. None of us have crystal balls, otherwise I would be in Monte Carlo right now with all the other millionaires...

Both shares are growth shares, with BNB yet to clarify its P/E a bit more (hopefully this December 2005 full year result). Both have had a number of earnings upgrades, with BNB expected to produce a circa $216 million full year profit, following two 20% upgrades. The prospectus forecasted

$154.7 million. BNB's P/E appears to be a little more expensive than MBL's following the respective guidances, but both companies have said their guidances would be "at least" the forecasts made. BNB, with its GPT joint venture or potentially other initiatives, could potentially pull even more income out of the bag, making its P/E look better again. Both companies have been very busy doing further deals globally this year, which are longer term deals, to snowball in the context of future earnings.

Both have been said to deserve the same P/E valuation on the basis that BNB's better growth prospects offset its higher balance sheet risk. On the upside, you could argue BNB has a lot more growth potential, by looking at its trading performance thus far, over and above MBL, which trades on a lower P/E.

Bar the shouting, both these growth shares should do well in buoyant market conditions. Indeed, their very business models are interrelated to the health of the global/Australian economy/markets.

As MBL does well, BNB seems to do even better, to show what it can become. BNB also appears to be even more internationally focussed, which is the next major frontier for MBL's continued growth outside its home market.

In a downturn, the recent October 2005 crunch showed how resilient each share may be in inevitably tougher times. BNB was hurt more than MBL, but did rebound better from its $15 low (helped by the fact it fell more). MBL is better diversified in its operations, while BNB is more specialised and following a mini-mac model.

Both have strong and growing long-term cash flows from global, market-leading assets, to buffer bad times. Such cash flows ensure debt levels are manageable, as do efforts to fix debt interest rates to counter future increases.

MBL's tilt at the LSE and other growing global moves represent the company's next major growth watershed, and should be expected to underpin the continued march of its share price. Of course, what is to stop BNB doing this, or should I say, continuing to follow a similar sounding strategy? BNB may well just be in "catch up", then "pass by" mode. For the present, BNB requires a greater risk appetite in tougher markets, to go with the benefits of its to-date greater finesse during good markets.

-----------------------------------------------------------------------

These are just my own thoughts, not recommendations to you. I am not qualified to give investment advice!

RichKid

PlanYourTrade > TradeYourPlan

- Joined

- 18 June 2004

- Posts

- 3,031

- Reactions

- 5

Re: MBL vs BNB- which is best?

Great summary waytogo,

I guess BNB is clearly more volatile atm as you say (and as the charts show) and a lot will depend on how the market fares as they are exposed to many listed vehicles. I've heard that increasing interest rates (which I think is a done deal over the coming years) may be a vulnerability for both stocks. Not sure how far that is true as I assume they would have hedged that risk to some degree.

waytogo said:Which is best - your own answer to this question may come down simply to your risk/reward appetite. Some thoughts I had follow- bear in mind my comments are speculative in nature, and you must make your own investment choice. None of us have crystal balls, otherwise I would be in Monte Carlo right now with all the other millionaires...

Great summary waytogo,

I guess BNB is clearly more volatile atm as you say (and as the charts show) and a lot will depend on how the market fares as they are exposed to many listed vehicles. I've heard that increasing interest rates (which I think is a done deal over the coming years) may be a vulnerability for both stocks. Not sure how far that is true as I assume they would have hedged that risk to some degree.

Re: MBL vs BNB- which is best?

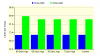

BNB

FORECAST EARNINGS Last Analyst Update

29 December, 2005

EPS(c) PE Growth

Year Ending 30-12-05 71.1 24.1 235.0%

Year Ending 30-12-06 86.4 19.8 21.5%

FORECAST EARNINGS TREND DETAILS

Year Ending 30-12-05 --------- Year Ending 30-12-06

EPS(c) PE Growth --------- EPS(c) PE Growth

Median 71.1 24.1 235.0% 86.4 19.8 21.5%

High 76.3 22.4 259.5% 92.3 18.5 21.0%

Low 65.9 25.9 210.5% 80.5 21.2 22.2%

30 Days Ago 71.1 86.4

60 Days Ago 71.1 86.4

90 Days Ago 71.0 89.5

Number of Analyst

Estimates 2 2

FORECAST EARNINGS TREND

Have the analysts been upgrading or downgrading their forecasts over the last 3 months?

BNB

FORECAST EARNINGS Last Analyst Update

29 December, 2005

EPS(c) PE Growth

Year Ending 30-12-05 71.1 24.1 235.0%

Year Ending 30-12-06 86.4 19.8 21.5%

FORECAST EARNINGS TREND DETAILS

Year Ending 30-12-05 --------- Year Ending 30-12-06

EPS(c) PE Growth --------- EPS(c) PE Growth

Median 71.1 24.1 235.0% 86.4 19.8 21.5%

High 76.3 22.4 259.5% 92.3 18.5 21.0%

Low 65.9 25.9 210.5% 80.5 21.2 22.2%

30 Days Ago 71.1 86.4

60 Days Ago 71.1 86.4

90 Days Ago 71.0 89.5

Number of Analyst

Estimates 2 2

FORECAST EARNINGS TREND

Have the analysts been upgrading or downgrading their forecasts over the last 3 months?

Attachments

Re: MBL vs BNB- which is best?

MBL

FORECAST EARNINGS Last Analyst Update

29 December, 2005

EPS(c) PE Growth

Year Ending 30-03-06 401.3 16.9 23.9%

Year Ending 30-03-07 437.9 15.5 9.1%

FORECAST EARNINGS TREND DETAILS

Year Ending 30-03-06 --------- Year Ending 30-03-07

EPS(c) PE Growth --------- EPS(c) PE Growth

Median 401.3 16.9 23.9% 437.9 15.5 9.1%

High 410.7 16.6 26.8% 459.4 14.8 11.9%

Low 379.0 17.9 17.0% 374.1 18.2 -1.3%

30 Days Ago 394.6 437.9

60 Days Ago 377.5 414.5

90 Days Ago 373.0 411.1

Number of Analyst

Estimates 6 6

FORECAST EARNINGS TREND

Have the analysts been upgrading or downgrading their forecasts over the last 3 months?

MBL

FORECAST EARNINGS Last Analyst Update

29 December, 2005

EPS(c) PE Growth

Year Ending 30-03-06 401.3 16.9 23.9%

Year Ending 30-03-07 437.9 15.5 9.1%

FORECAST EARNINGS TREND DETAILS

Year Ending 30-03-06 --------- Year Ending 30-03-07

EPS(c) PE Growth --------- EPS(c) PE Growth

Median 401.3 16.9 23.9% 437.9 15.5 9.1%

High 410.7 16.6 26.8% 459.4 14.8 11.9%

Low 379.0 17.9 17.0% 374.1 18.2 -1.3%

30 Days Ago 394.6 437.9

60 Days Ago 377.5 414.5

90 Days Ago 373.0 411.1

Number of Analyst

Estimates 6 6

FORECAST EARNINGS TREND

Have the analysts been upgrading or downgrading their forecasts over the last 3 months?

Attachments

- Joined

- 23 June 2005

- Posts

- 608

- Reactions

- 3

Re: MBL vs BNB- which is best?

I have my eye on mbl installment warrants, however, i wont be in one bank but most likely the majority of them with different weightings for each one of them.

I like mbl as it is the only growth stock with a near frundamental p/e and there is no economic indication that they will not continue to grow earnings.

I like st george because it has the least market capitalisation and would be one of the most potentail take over targets.

I like NAB because when this baby recovers it most likely will recover with lightening speed, the trouble is about when, so you got to have your money there as any fundmanager who misses out will get their back side kicked.

ANZ and CBA have given no indication that they are not going to continue growing earnings and any of the two will most likely be involved in a take over offensive of St george and to a lesser extent AMP.

Suncorp metway i like because they are another type of QBE story but a bank as well, so diversity diversity

I have my eye on mbl installment warrants, however, i wont be in one bank but most likely the majority of them with different weightings for each one of them.

I like mbl as it is the only growth stock with a near frundamental p/e and there is no economic indication that they will not continue to grow earnings.

I like st george because it has the least market capitalisation and would be one of the most potentail take over targets.

I like NAB because when this baby recovers it most likely will recover with lightening speed, the trouble is about when, so you got to have your money there as any fundmanager who misses out will get their back side kicked.

ANZ and CBA have given no indication that they are not going to continue growing earnings and any of the two will most likely be involved in a take over offensive of St george and to a lesser extent AMP.

Suncorp metway i like because they are another type of QBE story but a bank as well, so diversity diversity

michael_selway

Coal & Phosphate, thats it!

- Joined

- 20 October 2005

- Posts

- 2,397

- Reactions

- 2

Re: MBL vs BNB- which is best?

Hi can u tell me what the "QBE story" is

thanks!

TheAnalyst said:Suncorp metway i like because they are another type of QBE story but a bank as well, so diversity diversity

Hi can u tell me what the "QBE story" is

thanks!

RichKid

PlanYourTrade > TradeYourPlan

- Joined

- 18 June 2004

- Posts

- 3,031

- Reactions

- 5

Re: MBL vs BNB- which is best?

Please keep this on topic folks, by all means start a new thread if need be for Suncorp....

michael_selway said:Hi can u tell me what the "QBE story" is

thanks!

Please keep this on topic folks, by all means start a new thread if need be for Suncorp....

Re: MBL vs BNB- which is best?

please define "on topic"

RichKid said:Please keep this on topic folks, by all means start a new thread if need be for Suncorp....

please define "on topic"

- Joined

- 23 June 2005

- Posts

- 608

- Reactions

- 3

Re: MBL vs BNB- which is best?

Let me guess! you are related to chicken......lol...

michael_selway said:Hi can u tell me what the "QBE story" is

thanks!

Let me guess! you are related to chicken......lol...

RichKid

PlanYourTrade > TradeYourPlan

- Joined

- 18 June 2004

- Posts

- 3,031

- Reactions

- 5

Re: MBL vs BNB- which is best?

Thanks for the question. The title of the thread is always a useful guide. This thread is not about all banks, it's about how MBL & BNB compare to each other.

Waytogo's post is a good example of the comparative analysis which we seek in this thread. Posts on MBL or BNB alone can go in the MBL or BNB threads. Hope that it is clear now, your posts comparing the financials of each bank is great for fleshing out the points raised earlier by Waytogo.

brisvegas said:please define "on topic"

Thanks for the question. The title of the thread is always a useful guide. This thread is not about all banks, it's about how MBL & BNB compare to each other.

Waytogo's post is a good example of the comparative analysis which we seek in this thread. Posts on MBL or BNB alone can go in the MBL or BNB threads. Hope that it is clear now, your posts comparing the financials of each bank is great for fleshing out the points raised earlier by Waytogo.

Re: MBL vs BNB- which is best?

Reading through newspapers, MBL has featured fairly consistently as a key pick for the new year, with BNB expected to again go over $20 in 2006, after its recent pasting. Based on buoyant markets and continued global growth, MBL's (and BB's) successful business model should reasonably produce such results.

MBL (and BNB) are following a strategic growth theme, which is ramping up

global asset acquisitions into the upward global economic cycle. Allan Moss’ stategy is to pursue “big opportunities in big markets”.

Sure interest rates spook the market (and probably BNB more than MBL given its greater volatility), and yes interest rate rises are the biggest threat to both stocks, but rising interest rates are also a very positive sign of healthy economic growth/its accompanying CPI pressure. The healthy global economic growth will be MBL's/BNB's meal ticket. Central banks around the world need to carefully ensure they don't increase interest rates too far though, and smother the valuable growth.

MBL and BNB's other three major risks to earnings and share price growth are declining equity markets, competition for assets being purchased and sentiment. MBL has a reasonable exposure to poor sentiment, given fee criticism in the past, and the public nature of several assets like the tollways and airports. So, sentiment is probably their no. 2 risk. Various catchphrases that praise the 'Millionaires Factory' just as easily get trotted out in damaging media articles when newspaper sales are needed with the help of emotive articles. I think most people wuld be surprised if an organisation like MBL wasn't trying to earn fees from its line of business.

I am not qualified to give financial advice - you should seek your own recommendations.

Reading through newspapers, MBL has featured fairly consistently as a key pick for the new year, with BNB expected to again go over $20 in 2006, after its recent pasting. Based on buoyant markets and continued global growth, MBL's (and BB's) successful business model should reasonably produce such results.

MBL (and BNB) are following a strategic growth theme, which is ramping up

global asset acquisitions into the upward global economic cycle. Allan Moss’ stategy is to pursue “big opportunities in big markets”.

Sure interest rates spook the market (and probably BNB more than MBL given its greater volatility), and yes interest rate rises are the biggest threat to both stocks, but rising interest rates are also a very positive sign of healthy economic growth/its accompanying CPI pressure. The healthy global economic growth will be MBL's/BNB's meal ticket. Central banks around the world need to carefully ensure they don't increase interest rates too far though, and smother the valuable growth.

MBL and BNB's other three major risks to earnings and share price growth are declining equity markets, competition for assets being purchased and sentiment. MBL has a reasonable exposure to poor sentiment, given fee criticism in the past, and the public nature of several assets like the tollways and airports. So, sentiment is probably their no. 2 risk. Various catchphrases that praise the 'Millionaires Factory' just as easily get trotted out in damaging media articles when newspaper sales are needed with the help of emotive articles. I think most people wuld be surprised if an organisation like MBL wasn't trying to earn fees from its line of business.

I am not qualified to give financial advice - you should seek your own recommendations.

Re: MBL vs BNB- which is best?

Jeff B highlighted the strong resistance keeping MBL below $64 on 3 August 2005. What's the price today? $63-odd.

MBL has had quite a lot of trouble staying past $64, not to mention dipping below $60 a few times too, over the last 11 months.

What is it with Macquarie? It's had plenty of deal announcements, and not excessive negative media coverage.

Can it's dismal SP performance just be put down to choppy equity markets and the difficulty moving assets off its balance sheet to recycle profits? Profit levels have been at a record anyway. The 2007 full year result will include Dyno Nobel and the $90M profit from the sale of its stake in Macquarie Goodman. It isn't hard to roughly work out their profit this time will exceed $1 Billion. They are snowballing in size globally, so even this figure should keep rolling.

BNB is doing well, putting out more profit upgrades, around eight in the space of two years' listing. It's admittedly been a little range bound too, having trouble getting past $20, but managing to quickly recoup its major fall down to $15 during last year's October correction.

Is it MBL's big share price that's holding it back, while the more nimble BNB has a strong growth path? BNB has achieved the same growth it took MBL the last four years to achieve. BNB has done it in 2 years of listing.

BNB has gone down the same track of setting up specialist funds and truly is a mini-mac. But will it be a victim of its own growth and success like MBL later?

Jeff B highlighted the strong resistance keeping MBL below $64 on 3 August 2005. What's the price today? $63-odd.

MBL has had quite a lot of trouble staying past $64, not to mention dipping below $60 a few times too, over the last 11 months.

What is it with Macquarie? It's had plenty of deal announcements, and not excessive negative media coverage.

Can it's dismal SP performance just be put down to choppy equity markets and the difficulty moving assets off its balance sheet to recycle profits? Profit levels have been at a record anyway. The 2007 full year result will include Dyno Nobel and the $90M profit from the sale of its stake in Macquarie Goodman. It isn't hard to roughly work out their profit this time will exceed $1 Billion. They are snowballing in size globally, so even this figure should keep rolling.

BNB is doing well, putting out more profit upgrades, around eight in the space of two years' listing. It's admittedly been a little range bound too, having trouble getting past $20, but managing to quickly recoup its major fall down to $15 during last year's October correction.

Is it MBL's big share price that's holding it back, while the more nimble BNB has a strong growth path? BNB has achieved the same growth it took MBL the last four years to achieve. BNB has done it in 2 years of listing.

BNB has gone down the same track of setting up specialist funds and truly is a mini-mac. But will it be a victim of its own growth and success like MBL later?

michael_selway

Coal & Phosphate, thats it!

- Joined

- 20 October 2005

- Posts

- 2,397

- Reactions

- 2

Re: MBL vs BNB- which is best?

Basically not much growth for MBL % pa wise, atm, compared with BNB, AFG and MFS.

MBL - Earnings and Dividends Forecast (cents per share)

2006 2007 2008 2009

EPS 382.3 440.2 471.2 478.0

DPS 215.0 250.0 267.5 292.0

BNB - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS 77.0 106.3 130.5 156.3

DPS 23.0 33.0 41.0 48.5

AFG - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS 32.0 48.7 62.3 77.4

DPS 30.6 42.0 43.0 45.6

MFS - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS -6.8 24.4 30.0 39.2

DPS -- 14.0 18.5 23.5

thx

MS

bug said:Jeff B highlighted the strong resistance keeping MBL below $64 on 3 August 2005. What's the price today? $63-odd.

MBL has had quite a lot of trouble staying past $64, not to mention dipping below $60 a few times too, over the last 11 months.

What is it with Macquarie? It's had plenty of deal announcements, and not excessive negative media coverage.

Can it's dismal SP performance just be put down to choppy equity markets and the difficulty moving assets off its balance sheet to recycle profits? Profit levels have been at a record anyway. The 2007 full year result will include Dyno Nobel and the $90M profit from the sale of its stake in Macquarie Goodman. It isn't hard to roughly work out their profit this time will exceed $1 Billion. They are snowballing in size globally, so even this figure should keep rolling.

BNB is doing well, putting out more profit upgrades, around eight in the space of two years' listing. It's admittedly been a little range bound too, having trouble getting past $20, but managing to quickly recoup its major fall down to $15 during last year's October correction.

Is it MBL's big share price that's holding it back, while the more nimble BNB has a strong growth path? BNB has achieved the same growth it took MBL the last four years to achieve. BNB has done it in 2 years of listing.

BNB has gone down the same track of setting up specialist funds and truly is a mini-mac. But will it be a victim of its own growth and success like MBL later?

Basically not much growth for MBL % pa wise, atm, compared with BNB, AFG and MFS.

MBL - Earnings and Dividends Forecast (cents per share)

2006 2007 2008 2009

EPS 382.3 440.2 471.2 478.0

DPS 215.0 250.0 267.5 292.0

BNB - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS 77.0 106.3 130.5 156.3

DPS 23.0 33.0 41.0 48.5

AFG - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS 32.0 48.7 62.3 77.4

DPS 30.6 42.0 43.0 45.6

MFS - Earnings and Dividends Forecast (cents per share)

2005 2006 2007 2008

EPS -6.8 24.4 30.0 39.2

DPS -- 14.0 18.5 23.5

thx

MS

Similar threads

- Replies

- 31

- Views

- 4K

- Replies

- 10

- Views

- 4K