You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

This news was published 3 days ago on the ASX.....read it....Hi Chicken,

I am also a Metals X fan and just purchased in at .42c

How did you find out about the JP Morgan 50mill share buy ? I couldn't see these volumes. Were they purchased outside of the market ?

Is anyone here know who are selling and why they are selling MLX? I feel it is very strange for a share like this fall around 25%

It is backed up by JP morgan and Chinese investor.

It has large resource underground.

It has Ni and AL which is very hot commodity this year.

It is current producer of AL, the profit of this year could be astonishing.

I just do not get why ppl sell it.

I think the answer could be one or several of the following, not sure which one is the main reason.

1 better opportunity of other investment in the market

2 profit taking

3 market manipulating by JP morgan and they actually want more

4 some bad news approaching

5 seller is stupid

It is backed up by JP morgan and Chinese investor.

It has large resource underground.

It has Ni and AL which is very hot commodity this year.

It is current producer of AL, the profit of this year could be astonishing.

I just do not get why ppl sell it.

I think the answer could be one or several of the following, not sure which one is the main reason.

1 better opportunity of other investment in the market

2 profit taking

3 market manipulating by JP morgan and they actually want more

4 some bad news approaching

5 seller is stupid

I have had a crack at drawing a chart. To me it looks good. I dont really know much about charting but I have had a crack, because I think i am not far off the mark. I reckon we may have an opportunity to purchase in the high 30's for a short period of time, but I dont think 50 cents is to far away.

I can see MLX setting a new 52 week high, and we know that can spur on an extended run. Who knows?

I can see MLX setting a new 52 week high, and we know that can spur on an extended run. Who knows?

Attachments

- Joined

- 9 January 2006

- Posts

- 335

- Reactions

- 0

Thanks Ken.

Here is the gist of the Financial Review article today:

It is Southern Cross Equities director's top pick among the mid to small cap resource plays. MLX's assests include the Wingellina Prospect (N.T) & royalties payable by BHP from Kamgalda & Mount Keith (W.A) nickel fields. It also owns the Collingwood Tin project (Qld) & Renison Tin project (Tas).

According to AFR Aitken is extremely bullish on the SP prospects saying it looks cheap. He says the SP should double over the short to medium term & recommends "buying it aggressively under 50c".

Key to his strong outlook is the potential for Wingellina to drive MLX's longer-term eearnings & valuation, while the restart of the Renison Tin project is expected to have a significant impact on earnings.

Current SP is .425.

Here is the gist of the Financial Review article today:

It is Southern Cross Equities director's top pick among the mid to small cap resource plays. MLX's assests include the Wingellina Prospect (N.T) & royalties payable by BHP from Kamgalda & Mount Keith (W.A) nickel fields. It also owns the Collingwood Tin project (Qld) & Renison Tin project (Tas).

According to AFR Aitken is extremely bullish on the SP prospects saying it looks cheap. He says the SP should double over the short to medium term & recommends "buying it aggressively under 50c".

Key to his strong outlook is the potential for Wingellina to drive MLX's longer-term eearnings & valuation, while the restart of the Renison Tin project is expected to have a significant impact on earnings.

Current SP is .425.

Hey guys this one is well worth a look into major tin/nickel play very good institutional/chinese backers and well set to benefit from the surge in Tin prices. Also receiving large royalty from Kambalda/Bhp nickel operations already over $10.5 million this financial year and growing.

Really not surprising the strength of MLX today given the huge run up in Tin last night up $589 or 4.1%, with supply issues globally, MLX is very well placed to benefit from the rise in prices due to their current operations and by next year will be in the top 5 Tin producers worldwide.

With available shares drying up media starting to take a liking to the company, will not be surprised if it breaks the 50c barrier very shortly.

Good presentation with link below.

http://metalsx.com.au/investors/presentations/20070515Presentation.html

Really not surprising the strength of MLX today given the huge run up in Tin last night up $589 or 4.1%, with supply issues globally, MLX is very well placed to benefit from the rise in prices due to their current operations and by next year will be in the top 5 Tin producers worldwide.

With available shares drying up media starting to take a liking to the company, will not be surprised if it breaks the 50c barrier very shortly.

Good presentation with link below.

http://metalsx.com.au/investors/presentations/20070515Presentation.html

- Joined

- 31 October 2006

- Posts

- 739

- Reactions

- 0

Hey guys this one is well worth a look into major tin/nickel play very good institutional/chinese backers and well set to benefit from the surge in Tin prices. Also receiving large royalty from Kambalda/Bhp nickel operations already over $10.5 million this financial year and growing.

Really not surprising the strength of MLX today given the huge run up in Tin last night up $589 or 4.1%, with supply issues globally, MLX is very well placed to benefit from the rise in prices due to their current operations and by next year will be in the top 5 Tin producers worldwide.

With available shares drying up media starting to take a liking to the company, will not be surprised if it breaks the 50c barrier very shortly.

Good presentation with link below.

http://metalsx.com.au/investors/presentations/20070515Presentation.html

Agree Mick, I like the look of MLX too. May of missed a good buying op in the low 30's though. Seems to of found some strength in the depth.

Sean K

Moderator

- Joined

- 21 April 2006

- Posts

- 22,363

- Reactions

- 11,721

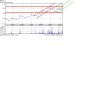

Potential breakout here and with general momentum and trending up, will have to happen some time sooner or later. Maybe most resistance at 44 cents, and a bit at all time intraday high at 45, so not much further to go. Should be pretty good support around 40 ish, possibly more at 37.5 ish worst case, which isn't too much downside.

Attachments

Thanks to both Ken and Kennas on the charts and the info, I have been watching MLX for a while and jumped aboard with a large stake yesterday.

Will post more indepth research over the weekend, but the main things that attracted me to the stock were.

1. The royalty received on the Kambalda/BHP nickel operations which is around $15 million per year with more deposits still to come online.

2. The fact they will be Australia's largest independent Tin producer with 1 operation already and 2 to come online shortly. Which will put them in the worlds top 6 producers.

3. They also control the worlds 16th largest undeveloped Nickel deposit which has attracted significant funds from China's largest Nickel producer and several large institutional investors. (with the Jinchuan Group aboard it is only a matter of time before the project is given the green light)

4. It is approaching the resistance at the 44c level with a massive increase in volume and if this was to break could quickly go on a bit of a run.(chart view kindly provided by Kennas)

Would be interested to hear peoples thoughts on the long term outlook for MLX

Will post more indepth research over the weekend, but the main things that attracted me to the stock were.

1. The royalty received on the Kambalda/BHP nickel operations which is around $15 million per year with more deposits still to come online.

2. The fact they will be Australia's largest independent Tin producer with 1 operation already and 2 to come online shortly. Which will put them in the worlds top 6 producers.

3. They also control the worlds 16th largest undeveloped Nickel deposit which has attracted significant funds from China's largest Nickel producer and several large institutional investors. (with the Jinchuan Group aboard it is only a matter of time before the project is given the green light)

4. It is approaching the resistance at the 44c level with a massive increase in volume and if this was to break could quickly go on a bit of a run.(chart view kindly provided by Kennas)

Would be interested to hear peoples thoughts on the long term outlook for MLX

interesting article I found on basemetals.com today pretty well sums up why TIN and inturn MLX has further upside from these levels.

Noticed it just hit 44.5c if we see some more buying this afternoon there is a real chance for a technical breakout on top of the fundamentals that are at play.

DJ BASE METALS: LME Tin Jumps On Technical Breakout

Wed, Jul 18 2007, 17:25 GMT

http://www.osterdowjones.com/

London Metal Exchange tin blitzed the rest of the complexWednesday as funds leaped at a technical play that market participants seedriving it higher.

LME tin jumped almost 5% Wednesday, to end just shy of $15,000/ton, short ofits $15,100/ton April high.

The metal has been traded around $14,000/ton since mid-May, traders said,which added fuel to the breakout, as buy stops were triggered at key technicallevels all the way up.

Already, analysts have warned of a "new nickel or lead" in the making, withtechnical indicators for the metal pointing as high as $16,000/ton, said UBSanalyst Robin Bhar.

Like the lead and nickel markets, the tin market is relatively small, withsupply side stresses, and dominated by one or two "very, very large funds,"analysts said.

In the coming days, LME tin is set to challenge$15,100/ton hit in April when Indonesian supply problems kicked in, market players said.

Indonesian authorities cracked down on dozens of small smelters last October,forcing them to close up shop due to environmental and tax code breaches,although some larger smelters have gradually come back on line.

Mostly due to these problems, reported tin production from January to May was down 2,900 tons on the year, the World Bureau of Metal Statistics said Wednesday.

Noticed it just hit 44.5c if we see some more buying this afternoon there is a real chance for a technical breakout on top of the fundamentals that are at play.

DJ BASE METALS: LME Tin Jumps On Technical Breakout

Wed, Jul 18 2007, 17:25 GMT

http://www.osterdowjones.com/

London Metal Exchange tin blitzed the rest of the complexWednesday as funds leaped at a technical play that market participants seedriving it higher.

LME tin jumped almost 5% Wednesday, to end just shy of $15,000/ton, short ofits $15,100/ton April high.

The metal has been traded around $14,000/ton since mid-May, traders said,which added fuel to the breakout, as buy stops were triggered at key technicallevels all the way up.

Already, analysts have warned of a "new nickel or lead" in the making, withtechnical indicators for the metal pointing as high as $16,000/ton, said UBSanalyst Robin Bhar.

Like the lead and nickel markets, the tin market is relatively small, withsupply side stresses, and dominated by one or two "very, very large funds,"analysts said.

In the coming days, LME tin is set to challenge$15,100/ton hit in April when Indonesian supply problems kicked in, market players said.

Indonesian authorities cracked down on dozens of small smelters last October,forcing them to close up shop due to environmental and tax code breaches,although some larger smelters have gradually come back on line.

Mostly due to these problems, reported tin production from January to May was down 2,900 tons on the year, the World Bureau of Metal Statistics said Wednesday.

well guys with the current focus on the LME on Lead/Tin prices what better time to have a closer look at MLX, Australia's largest Tin producer and as of 2008 the worlds 6th largest Tin producer.

Also they control the enormous Wingellina Nickel Deposit which is larger and higher grade than BHP's Ravensthorpe Nickel Project.

Now a closer looks at MLX

Shares 915,335,378

Options 20c 110,495,600

Current undiluted market cap $402 million

Reason to buy into the MLX story

-Current Nickel royalty from Mt Keith/Kambalda $16-20 million per year(at no cost to MLX)

-Currently producing Tin from Collingwood Project (exposure to rising tin prices)

-Production at Renison/Mt Bischoff Tin Projects late 2007

-Feasability Study underway Rentails Tin Project production early 2009

-Strong Cash Position

-Strong Institutional Support

-Top 6 Shareholder control 50% of company

-Massive upside through Wingellina Nickel Deposit (value aud $100 billion)

-Projected EBITDA 2008 $100 million or PE 4.4

A closer look at MLX Projects

Collingwood Tin

The Collingwood mineralisation is greisen style within granites. The mineralisation occurs as a series of close spaced sub parallel siliceous-sheeted greisen lodes that trend north-south and dip steeply east. Tin occurs within the lodes as granular, sub-spherical grains of cassiterite between 0.5mm and 2mm in diameter. Reserves estimates as of 30 June 2006 total 953,900 tonnes at 1.19% Sn with a larger resource base of 1,280,900t at 1.27% Sn.

Yearly Production 3500 tonnes Tin

Projected Earnings of $15-20 million per year (with upside due to tin price)

Renison/Mt Bischoff Tin

Renison Resources 6.61 MT @ 1.6% SN

Mt Bischoff Resources 1.90 MT @ 0.96% SN

It is MLX intention to restart the Renison Tin Concentrator and treat ore from both deposits from late 2007

Yearly Production 8500 tonnes Tin

Projected Earnings of $60 million per year (with upside due to tin price)

Rentails Project

The Rentails Project is based on the re-treatment of historic tailings from over 40 years of mining at the Renison Bell Mine. Metals X is completing a feasibility study into the extraction of tin using a combination of ultrafine gravity and floatation techniques to produce a low grade concentrate for fuming and generation of a higher grade and sale-able tin concentrate.

Rentails Tin Project - 17.9 MT @ 0.42% Sn

Due to commence production in 2009 at a rate of 6000 tonnes of tin per year

Wingellina Nickel

The monster project of MLX at an inground resource of over $100 billion it is no wonder that the Jinchuan Group of China (China's largest Nickel Producer) has taken a 13% stake in the company, and has first rights for any offtake agreement)

With a current resource of 213 mt @0.95% nickel and 0.074% Cobalt

A recent scoping study found that at commodity prices

$20,000 tonnes nickel

$15lb cobalt

Wingellina would have a NPV (8%) of $5.3 billion or $5.30 per share

And a yearly profit of around $330 million which is almost equal to MLX current market cap.

http://metalsx.com.au/pdf/1176344469.pdf

Current Nickel Royalty

Metals X has significant assets in the form of production royalty streams, payable by Australia's premier nickel producer BHP Billiton and sourced from two of the world's largest and most productive nickel fields being Kambalda and Mount Keith. In addition Metals X owns royalties over significant land positions in the Mt Keith district and covering large tracts of highly prospective nickel tenements (Kingston Royalty).

With the increase in volume over the last couple of weeks, I have no doubt that we have started to see a major re-rating of the stock, which is being driven by institutional buying and an increased focus due to the increased price of Tin (remember MLX is Australia's largest Tin producer), also the massive value of the Wingellina Nickel Deposit (bigger than BHP's Ravensthorpe)

Also they control the enormous Wingellina Nickel Deposit which is larger and higher grade than BHP's Ravensthorpe Nickel Project.

Now a closer looks at MLX

Shares 915,335,378

Options 20c 110,495,600

Current undiluted market cap $402 million

Reason to buy into the MLX story

-Current Nickel royalty from Mt Keith/Kambalda $16-20 million per year(at no cost to MLX)

-Currently producing Tin from Collingwood Project (exposure to rising tin prices)

-Production at Renison/Mt Bischoff Tin Projects late 2007

-Feasability Study underway Rentails Tin Project production early 2009

-Strong Cash Position

-Strong Institutional Support

-Top 6 Shareholder control 50% of company

-Massive upside through Wingellina Nickel Deposit (value aud $100 billion)

-Projected EBITDA 2008 $100 million or PE 4.4

A closer look at MLX Projects

Collingwood Tin

The Collingwood mineralisation is greisen style within granites. The mineralisation occurs as a series of close spaced sub parallel siliceous-sheeted greisen lodes that trend north-south and dip steeply east. Tin occurs within the lodes as granular, sub-spherical grains of cassiterite between 0.5mm and 2mm in diameter. Reserves estimates as of 30 June 2006 total 953,900 tonnes at 1.19% Sn with a larger resource base of 1,280,900t at 1.27% Sn.

Yearly Production 3500 tonnes Tin

Projected Earnings of $15-20 million per year (with upside due to tin price)

Renison/Mt Bischoff Tin

Renison Resources 6.61 MT @ 1.6% SN

Mt Bischoff Resources 1.90 MT @ 0.96% SN

It is MLX intention to restart the Renison Tin Concentrator and treat ore from both deposits from late 2007

Yearly Production 8500 tonnes Tin

Projected Earnings of $60 million per year (with upside due to tin price)

Rentails Project

The Rentails Project is based on the re-treatment of historic tailings from over 40 years of mining at the Renison Bell Mine. Metals X is completing a feasibility study into the extraction of tin using a combination of ultrafine gravity and floatation techniques to produce a low grade concentrate for fuming and generation of a higher grade and sale-able tin concentrate.

Rentails Tin Project - 17.9 MT @ 0.42% Sn

Due to commence production in 2009 at a rate of 6000 tonnes of tin per year

Wingellina Nickel

The monster project of MLX at an inground resource of over $100 billion it is no wonder that the Jinchuan Group of China (China's largest Nickel Producer) has taken a 13% stake in the company, and has first rights for any offtake agreement)

With a current resource of 213 mt @0.95% nickel and 0.074% Cobalt

A recent scoping study found that at commodity prices

$20,000 tonnes nickel

$15lb cobalt

Wingellina would have a NPV (8%) of $5.3 billion or $5.30 per share

And a yearly profit of around $330 million which is almost equal to MLX current market cap.

http://metalsx.com.au/pdf/1176344469.pdf

Current Nickel Royalty

Metals X has significant assets in the form of production royalty streams, payable by Australia's premier nickel producer BHP Billiton and sourced from two of the world's largest and most productive nickel fields being Kambalda and Mount Keith. In addition Metals X owns royalties over significant land positions in the Mt Keith district and covering large tracts of highly prospective nickel tenements (Kingston Royalty).

With the increase in volume over the last couple of weeks, I have no doubt that we have started to see a major re-rating of the stock, which is being driven by institutional buying and an increased focus due to the increased price of Tin (remember MLX is Australia's largest Tin producer), also the massive value of the Wingellina Nickel Deposit (bigger than BHP's Ravensthorpe)

looks like the price of Tin is surging again overnight, smashing through the previous record high. Could be a really huge day for MLX tomorrow.

Shanghai copper rises 2.3 pct, tin soars

Thu 19 Jul 2007, 6:49 GMT

[-] Text [+] By Richard Dobson

TAIPEI (Reuters) - Shanghai copper rose more than 2 percent on Thursday, buoyed by demand for physical material and industrial action at key mines in Latin America amid an already tight market and strong Chinese economic growth data.

Three-month tin on the London Metal Exchange hit an all-time high of $15,530 on the electronic Select trading system, extending gains the previous day as supply shortfalls spurred fund buying.

On the Shanghai Futures Exchange, the most active September copper futures contract rose 1,470 yuan or 2.3 percent to 65,940 yuan a tonne.

"London prices rose a little from yesterday, while it seems there is some demand for material in the spot market," said a Shanghai-based trader.

"But demand from consumers is not strong around these price levels. If London rises much further, Shanghai probably won't follow."

Shanghai spot copper prices ranged between 64,550 yuan and 64,800 yuan, up 900 yuan from the previous day, indicating increasing demand for physical material.

Copper for delivery in three months on the London Metal Exchange was at $7,835, rising from $7,825 at the close on Wednesday, when it gained $60.

Copper prices remain supported by continuing industrial action in key suppliers Chile and Peru, compounding an already tight market.

The World Bureau of Metal Statistics research group said on Wednesday that the global copper market was in deficit by 144,000 tonnes between January and May this year, reflecting lower supplies.

This compared with a revised surplus of 182,000 tonnes for the whole of 2006, the British-based analyst said in a monthly report.

According to the International Copper Study Group, world refined copper consumption outpaced production by 267,000 tonnes in the first four months of the year, compared with a surplus of 35,000 tonnes in the year-ago period.

LME stocks reversed a moderate two-day rise, falling 775 tonnes to 98,625 tonnes on Wednesday.

On the industrial action front, workers at Southern Copper's Peruvian operations may go on strike again after unions failed to reach an agreement over demands for better salaries, a union leader said on Wednesday.

Chilean copper giant Codelco said all operations at its Salvador division remained on hold on Wednesday due to a strike by workers who have surrounded the plant and are refusing to let people enter.

CHINA GROWTH

Also boosting sentiment was the announcement by China, the world's largest copper consumer, that annual GDP growth surged to 11.9 percent in the second quarter from 11.1 percent in the first three months, beating forecasts.

The data kept China's economy firmly on course for the fifth straight year of double-digit expansion, while consumer prices rose 4.4 percent in the 12 months to June, also exceeding forecasts and reinforcing expectations of further monetary tightening.

"Some investors are worried that the central government will release more measures to cool the economy," said analyst Pang Ying at a trading house Shenzhen Rongtop.

Beijing in recent years has implemented a series of measures to stem growth in overheated and energy-intensive sectors such as copper smelting.

In other metals, tin added over 3 percent to trade at $15,400 by 0701 GMT, fuelled by concerns about a shortfall in output from Indonesia, which accounts for one-third of the world's tin output.

In other metals, nickel added almost 2 percent to trade at $33,400, while lead was steady at $3,235 after hitting a new record of $3,260 a tonne on Wednesday on news of an explosion at a U.S. refinery last week

Shanghai copper rises 2.3 pct, tin soars

Thu 19 Jul 2007, 6:49 GMT

[-] Text [+] By Richard Dobson

TAIPEI (Reuters) - Shanghai copper rose more than 2 percent on Thursday, buoyed by demand for physical material and industrial action at key mines in Latin America amid an already tight market and strong Chinese economic growth data.

Three-month tin on the London Metal Exchange hit an all-time high of $15,530 on the electronic Select trading system, extending gains the previous day as supply shortfalls spurred fund buying.

On the Shanghai Futures Exchange, the most active September copper futures contract rose 1,470 yuan or 2.3 percent to 65,940 yuan a tonne.

"London prices rose a little from yesterday, while it seems there is some demand for material in the spot market," said a Shanghai-based trader.

"But demand from consumers is not strong around these price levels. If London rises much further, Shanghai probably won't follow."

Shanghai spot copper prices ranged between 64,550 yuan and 64,800 yuan, up 900 yuan from the previous day, indicating increasing demand for physical material.

Copper for delivery in three months on the London Metal Exchange was at $7,835, rising from $7,825 at the close on Wednesday, when it gained $60.

Copper prices remain supported by continuing industrial action in key suppliers Chile and Peru, compounding an already tight market.

The World Bureau of Metal Statistics research group said on Wednesday that the global copper market was in deficit by 144,000 tonnes between January and May this year, reflecting lower supplies.

This compared with a revised surplus of 182,000 tonnes for the whole of 2006, the British-based analyst said in a monthly report.

According to the International Copper Study Group, world refined copper consumption outpaced production by 267,000 tonnes in the first four months of the year, compared with a surplus of 35,000 tonnes in the year-ago period.

LME stocks reversed a moderate two-day rise, falling 775 tonnes to 98,625 tonnes on Wednesday.

On the industrial action front, workers at Southern Copper's Peruvian operations may go on strike again after unions failed to reach an agreement over demands for better salaries, a union leader said on Wednesday.

Chilean copper giant Codelco said all operations at its Salvador division remained on hold on Wednesday due to a strike by workers who have surrounded the plant and are refusing to let people enter.

CHINA GROWTH

Also boosting sentiment was the announcement by China, the world's largest copper consumer, that annual GDP growth surged to 11.9 percent in the second quarter from 11.1 percent in the first three months, beating forecasts.

The data kept China's economy firmly on course for the fifth straight year of double-digit expansion, while consumer prices rose 4.4 percent in the 12 months to June, also exceeding forecasts and reinforcing expectations of further monetary tightening.

"Some investors are worried that the central government will release more measures to cool the economy," said analyst Pang Ying at a trading house Shenzhen Rongtop.

Beijing in recent years has implemented a series of measures to stem growth in overheated and energy-intensive sectors such as copper smelting.

In other metals, tin added over 3 percent to trade at $15,400 by 0701 GMT, fuelled by concerns about a shortfall in output from Indonesia, which accounts for one-third of the world's tin output.

In other metals, nickel added almost 2 percent to trade at $33,400, while lead was steady at $3,235 after hitting a new record of $3,260 a tonne on Wednesday on news of an explosion at a U.S. refinery last week

- Joined

- 31 October 2006

- Posts

- 739

- Reactions

- 0

Thanks mick for you research. I've held off buying MLX for a while now, was very tempted to at 35 cents  . If it breaks 44 cents and the resistance dissapears, i'll take the plunge. Hope i'm not too late.

. If it breaks 44 cents and the resistance dissapears, i'll take the plunge. Hope i'm not too late.

. If it breaks 44 cents and the resistance dissapears, i'll take the plunge. Hope i'm not too late.hi Pat, according to the Southern Cross Equities team there is plenty of upside left, they have rated it their most outstanding buy, with plenty of upside left.

It gets better everytime I check kitcometals.com or basemetals.com there is another article about how tin is surging to record highs.

It is just a matter of time before investors put two and two together and realise MLX is the best Tin leveraged stock on the ASX.

It gets better everytime I check kitcometals.com or basemetals.com there is another article about how tin is surging to record highs.

It is just a matter of time before investors put two and two together and realise MLX is the best Tin leveraged stock on the ASX.

- Joined

- 31 October 2006

- Posts

- 739

- Reactions

- 0

I just feel that i've missed out on 20%, I've had MLX on my watchlist for some time and new it was a buy at 35 cents. Hindsight for you.hi Pat, according to the Southern Cross Equities team there is plenty of upside left, they have rated it their most outstanding buy, with plenty of upside left.

It gets better everytime I check kitcometals.com or basemetals.com there is another article about how tin is surging to record highs.

It is just a matter of time before investors put two and two together and realise MLX is the best Tin leveraged stock on the ASX.

There's so much resistance on depth i'll wait for a better opportunity.

I think investors have put 2 and 2 together.

MLX is flying. I reckon 46 cents is highly likely but with the article tonight about tin prices soaring it could really run.

Will wait and see what happens. Could be a very good Friday, lets hope the US market goes well.

MLX is flying. I reckon 46 cents is highly likely but with the article tonight about tin prices soaring it could really run.

Will wait and see what happens. Could be a very good Friday, lets hope the US market goes well.