- Joined

- 13 February 2006

- Posts

- 5,389

- Reactions

- 12,522

Timmy.

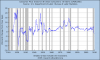

There is nothing incorrect with what I said, velocity has fallen off a cliff, no velocity, no inflation. When banks take those excess reserves, start to increase lending, stop tightening lending standards and businesses and households start to borrow more you'll get inflation.

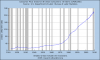

Duc, curious why the inflation chart you show from the Atlanta Fed shows a kick-up in inflation on the right-hand extreme whereas all other charts of US inflation are showing continued falls. Is the right-hand extreme on the Fed charts a projection?

Incorrect.

Velocity has fallen off a cliff. That represents the demand for currency, as credit has contracted, which, I agree is deflationary.

However, the contraction in bank credit, is being offset by an expansion in government credit via deficit spending. The result are the data points in the first set of charts.

Currently deflation is a non-event.

Forget about the graphs.... You only have to look at your utlility bills,supermarket shopping and day to day expenses to see if we are sitting in an inflationary or deflationary scenario (talking about here in Australia)

Plasma TV's - price down

Apple Mac - price down

Cars - price down

Inflation for the year to June was 1.5% (WWW.RBA.GOV.AU), so overall modest inflation, but decelerated very rapidly. Doubt we will go to deflation though - probably very low inflation for a while

Plasma TV's - price down

Apple Mac - price down

Cars - price down

My Rent - price up :frown:

Food - price up

Insurance - price up

My Rent - price up :frown:

Again, nothing incorrect in what I said, currently inflation is the non-event. We shall see in the coming years if that remains the case.

Duc, curious why the inflation chart you show from the Atlanta Fed shows a kick-up in inflation on the right-hand extreme whereas all other charts of US inflation are showing continued falls. Is the right-hand extreme on the Fed charts a projection?

Apart from your opinion, do you actually have any data that supports your assertion?

You know I'm sure the old adage - opinions are like assholes, everyone has one

As we all know duc, given your track record of opinions, yours is worth less than an asshole, but lets indulge your latest fantasy for a bit.

My opinion doesn't differ a whole lot. Yes the Fed and every other central bank have adopted an inflationary stance, clearly represented by the ballooning balance sheet of the Fed in the case of the US. This is undoubtedly inflationary as that excess liquidity makes it's way into the economy. However it is the last point that is not happening. Excess reserves held at the Fed have grown proportionately with the growth in the Fed's balance sheet. Also, the velocity of money in the economy has dried up.

On the deflationary side you have a deleveraging household sector which has shed approximately $14 trillion in net worth, is reducing debt and increasing savings. The corporate sector also continues to deleverage.

So we have a deflationary household and corporate sector and an inflationary Fed coupled with a dose of fiscal recklessness on the part of the congress. I can easily see how that translates into inflation 3-4 years out, but it is currently not evident.

Obviously touched a raw nerve there judging from your rather aggressive reply.

You accept that Central Banks worldwide have adopted an inflationary policy response. You also accept that in the future, unless this policy stance is reversed, that inflation will be the result.

Thus all that remains is the current timeframe.

You state that $14 trillion of net wort has been lost through asset price collapse. Agreed.

You state that the consumer is reducing debt.

Incorrect, look at the data. Consumer debt has only reduced by some 2% I'll post the exact numbers when I get back to my computer.

The Corporate sector is deleveraging via liquidation. This is not deflationary, this is inflationary. As capital is liquidated and stages of production curtailed, production is reduced.

Reduced production reduces supply. Reduced supply, in the face of stable demand, think necessities, food, power, etc, results in higher prices.

Demand is stable because the government is increasing government spending via deficits. These deficits are being expended within Welfare, Shovel ready, bailouts, etc.

The government borrowing and printing [via QE] is replacing consumer borrowing, thus, again the inflationary pressure is obvious in the data [refer to earlier charts]

The banks are simply not the correct place to be looking for the inflationary entry point. They were the credit creators in the last inflationary cycle, not this one however.

Thus I am not actually providing an "opinion" at all, rather simply elucidating the data for you.

Thanks for your attempts at elucidation duc, but at the end of the day you are, like everybody else, just pushing a point of view. Unfortunately it is just not very convincing.

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.