- Joined

- 13 September 2013

- Posts

- 988

- Reactions

- 531

where's the code?

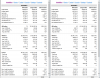

This is my results on my code 2016-now

clearly a single run but you get a idea

This is my results on my code 2016-now

clearly a single run but you get a idea