- Joined

- 19 October 2005

- Posts

- 4,859

- Reactions

- 7,313

GOR Taking up all its entitlement does not entail non dilution

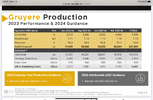

Well not to get into it too much until I bother to confirm for myself what is rumour at my level, but on the face of it I don't see why anyone would compliment GOR management on performance. Other than discover and define the deposit where is performance? They did not build the mine and plant, they are not active partners in the mining and they have not converted the large passive cashflow into notable new discovery.Performance has been pleasing so I won’t be making waves.

i don't HATE GOR , i just don't love it enough to buy more at the current pricesEverybody hate this GOR especially all BO system traders

What’s the issue with the hatred of GOR.Everybody hate this GOR especially all BO system

lived through a similar phase with OZ Minerals , took a lot of faith , the courage to buy into the slides , etc etc eventually got myself into a very nice position .. and along came BHP and all i got was a wad of cash ( and more issues in BHP )What’s the issue with the hatred of GOR.

I don’t trade it I hold it, I think if it meets its production targets and AISC doesn’t run away it could achieve $2.00 again.

I can understand the frustration that same may have trading GOR with its frequent sudden drops.

I would if I had spare.am currently up more than 35% on this one

feel free to buy my share ( of the cheaper GOR shares available today )

i put some of 'my spare ' into extra MGX todayI would if I had spare.

Dividend payment day today.I think the GOR so has been extremely disappointing considering the gold price.

Anyone else see why the sp hasn’t risen a lot more?

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.