skc

Goldmember

- Joined

- 12 August 2008

- Posts

- 8,277

- Reactions

- 329

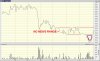

SP has bounced pretty hard off 35 cents. Currently back up at 42 cents.

So_Cynical, Ves, what are your takes on the situation? Have there been any positive news articles or research in the past week or two which indicate any recovery in sales?

I wonder if the Fonterra announcement of reduced farm gate milk price has anything to do with it...