Stormin_Norman

Currency Trader

- Joined

- 12 January 2008

- Posts

- 1,256

- Reactions

- 0

Just wondering if it's possible to code in allowance for certain time's of the day

yep. simple.

Just wondering if it's possible to code in allowance for certain time's of the day

sounds like the futures is a more efficient market .... but there are more trading opportunities in an inefficient marketThe difference is, one is run by a bunch of market makers on an unregulated market which it is basically impossible to get accurate volume for, and the other is on a regulated market, with a significantly reduced counter party risk, with a growing number of participants and where volume can be measured.

")

sounds like the futures is a more efficient market .... but there are more trading opportunities in an inefficient market

I guess there's heaps of arb robots already exploiting the typical divergences between spot and futures?

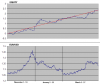

the EURJPY looks the most promising, but what's the difference between the two graphs: is that different versions of the EA, different data providers, or different time periods?so far 5m timeframe tests have been done on a few major pairs.

But you have people using futures to hedge currency risk, thus creating inefficiencies

I guess there's heaps of arb robots already exploiting the typical divergences between spot and futures?

the EURJPY looks the most promising, but what's the difference between the two graphs: is that different versions of the EA, different data providers, or different time periods?

latest version:

10k to about 300k in 4 years non compounding on AUDUSD (one market).

more work yet to do.

Why is it called "franklin - fixed exit v2" ..... it looks to me that your system moves its stop losses to break even..?

That drawdown at trade 148 must of hurt

Hello and welcome to Aussie Stock Forums!

To gain full access you must register. Registration is free and takes only a few seconds to complete.

Already a member? Log in here.