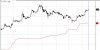

I've attached a chart to better show what I'm trying to do. The blue linear regression line on the attached chart obviously fits the current trend much better than the red regression line - the standard error is lower for the blue line (those are standard error channels on the chart).

I want Amibroker to calculate the regression periods length that best fits the current trend for each stock/chart. My thoughts are that StdErr may be a good way to do this, as StdErr should be lowest for the best fit line.

Any thoughts?

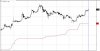

I want Amibroker to calculate the regression periods length that best fits the current trend for each stock/chart. My thoughts are that StdErr may be a good way to do this, as StdErr should be lowest for the best fit line.

Any thoughts?

(Eg. AAG says 275 bars when it should be 26)

(Eg. AAG says 275 bars when it should be 26)