- Joined

- 14 March 2006

- Posts

- 3,630

- Reactions

- 5

Re: COK - Cockatoo Coal

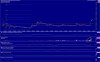

Cheers for the chart wl1.

Great to see COK firming up out of its flacid slumber. Also great to see it firming and shooting to the upside.

Also great to see it firming and shooting to the upside.

DISC: Still holding COK.

Wedge breaking to the upside on good volume, with no ann out would suggest a technical break out. Maybe on the expectations of an ANN

Chart can be view here!

From their last presentation "no cap raises" to be concerned about as will be self funding this year as a producer

LOOKING AHEAD

• In production

• Self-funded outlook for 2010/2011

• 50% production growth next 2-3 years requires no new major infrastructure/capital

• Major coal buyers hold strategic shareholdings

• PCI/Thermal assets - aligned to global demand growth

• 3-5 year target - establish position as significant, independent producer

• 2010 coal price forecasts rising

Cheers for the chart wl1.

Great to see COK firming up out of its flacid slumber.

Also great to see it firming and shooting to the upside. DISC: Still holding COK.