I still think that's MCR a good, well run, comparatively low cost operator. And the recent profit up-date does nothing to change that.

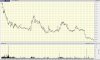

But the outlook for the PoN doesn't inspire confidence. LME stocks are still increasing, now at over 160,000 mt, highest level for at least 15 years.

Difficult to call a low in the SP in these circumstances, IMO.

But the outlook for the PoN doesn't inspire confidence. LME stocks are still increasing, now at over 160,000 mt, highest level for at least 15 years.

Difficult to call a low in the SP in these circumstances, IMO.

")