Here the emphasis is on the poor implementation of the investment philosophy (and lack of understanding of these "mum and dad" investors) rather than the actual strategy itself.The great majority of people who adopt a buy and hold approach do so either via an index fund or by taking a representative group of popular 'mum and dad' shares. They are the people who are still well and truly down in their Super accounts because they didn't consider the possibility of selling when they could hold on to most of their profits.

The two are often easy to confuse, but there is a subtle difference. The skill is not so much in being able to "buy and hold" but being able to "buy and hold the right shares."

Put it this way: if I was a technical analyst and got whipsawed constantly, missed every high and did not sell at every low - is it the fault of that method, or is it the implementation of that method?

Did you know that there are lots of good companies that are trading higher than they were before the GFC and you had plenty of dividend income with which to re-invest back into them at their lows? It's not all doom and gloom out there, you know!

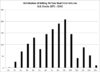

Do you not agree that a 9% annual return on the ASX accumulation index for the last ten years is something that should not be scoffed at so quickly?

The longer period of time over which you invest, and the more that you invest incrementally over that period of time, the more annual liquidity you will be able to draw on. What starts small acorn can grow into a very big tree within an investing career. There are most likely people who now earn an annual income greater than the original sum that they started with.If you'd sold $1M worth of shares reasonably close to the peak, I doubt an amount you're keeping in 'liquidity' is going to be equivalent in terms of purchasing power.

")