You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

CBA - Commonwealth Bank of Australia

- Thread starter stefan

- Start date

- Joined

- 23 October 2005

- Posts

- 859

- Reactions

- 0

Wavepicker, would you care to explain how you get the Fib date of 18 Feb and 11 Mar for CBA ? 18 Feb is its ex-div date for $1.13 so target of $44.2-45 is achievable.

Hello josjes,

Thanks for the Divvy info, had no idea it was due and adds more weight to the analysis.

I have very strong Fib Clusters at both 18th Feb and 11th March. Don't have time to post how those dates were calculated ATM, but will do so perhaps tommorow. The 11th March date seems to coincide nicely the analysis made in the XAO Analysis thread a weeks ago, see links below:

https://www.aussiestockforums.com/forums/showpost.php?p=258027&postcount=2842

https://www.aussiestockforums.com/forums/showpost.php?p=258028&postcount=2843

Cheers

This one has been battered of late. Looks like it maybe coming into a low in the next few days for it's biggest countertrend rally since the decline started. A clear 5 wave decline almost complete as well as a Fib turn date for 18th Feb and another critical one on the 11th March(along with the broader market)

Let's see how it goes the next coupe of days...

CBA goes ex-div tomorrow, so I don't like your chances of it turning tomorrow. Dividend is $1.13 fully franked

- Joined

- 23 October 2005

- Posts

- 859

- Reactions

- 0

CBA goes ex-div tomorrow, so I don't like your chances of it turning tomorrow. Dividend is $1.13 fully franked

To the contrary, it's perfect. What we want to see is a fall into that date. If it falls into that date chances are it might see the low tommorow. My dates are plus or minus a day, the reason for this is because it depends what time of the day a high or actually occured in the past that determines the future probability. A turn in the morning for example 2-3 months ago, can add an extra day when doing fibonacci expansions in forward timeframes.

- Joined

- 17 January 2007

- Posts

- 2,986

- Reactions

- 32

To the contrary, it's perfect. What we want to see is a fall into that date. If it falls into that date chances are it might see the low tommorow. My dates are plus or minus a day, the reason for this is because it depends what time of the day a high or actually occured in the past that determines the future probability. A turn in the morning for example 2-3 months ago, can add an extra day when doing fibonacci expansions in forward timeframes.

Well we got the ex div sell off plus a little bit more overcorrection (4365), presenting what I think is a pretty good short term trade, and I have taken positions at these levels for a 'sympathy'? rally, which is happening as I type. Extraordinary times but opportunities to go long are always there.

From the top @ 62 it's fallen some 30% or more in 3 months. Something about throwing the baby out with the bathwater? Put it this way, if CBA tanks from here we are all in big trouble as it would imply the global shake-out has finally hit Oz in a tangible way.

WP, is your upside target and timescale $50 plus on/near 11.3?

- Joined

- 8 November 2007

- Posts

- 314

- Reactions

- 0

I agree, overboard indeed. But it's more just the market factoring in a "worst case scenario" price, so any positive news during this period will lead to big rallies. For I remember about a month ago, there was a day when the market went down yet the biggest gainers on the ASX200 were CBA, ANZ and NAB -- something extremely rare.Well we got the ex div sell off plus a little bit more overcorrection (4365), presenting what I think is a pretty good short term trade, and I have taken positions at these levels for a 'sympathy'? rally, which is happening as I type. Extraordinary times but opportunities to go long are always there.

From the top @ 62 it's fallen some 30% or more in 3 months. Something about throwing the baby out with the bathwater? Put it this way, if CBA tanks from here we are all in big trouble as it would imply the global shake-out has finally hit Oz in a tangible way.

WP, is your upside target and timescale $50 plus on/near 11.3?

Strange times we live in, indeed. Record profits, record dividend payments, yet exaggerated selling. You can't win in these market conditions.

If it goes down again tomorrow I'm definitely gonna buy some, CBA @ $44.00 is overdone, hasn't seen that price since at least mid-2006.

- Joined

- 31 May 2006

- Posts

- 1,941

- Reactions

- 2

sounds like knife catching to me. As stated earlier in the thread - the comparitive attraction of the banks high yield diminishes as interest rates rise, and the banks are also facing various other risks at the moment. I've still got an open short position (partly closed the other day to cover the cost so the rest is free carried) - until it retraces I'll keep it open - there's no reason why it can't keep going down imo - so I'll stick with the trend for the time being until it retraces or volatility drops off.

- Joined

- 8 November 2007

- Posts

- 314

- Reactions

- 0

$1.13 fully franked dividend at $44.00 a stock? Are you for real? This is a great stock, CBA has been a proven performer for over a decade, and if any bank can ride out this turbulence, it's this one. I personally think this price is cheap, as are many banks, and am accumulating them because, eventually, they're going to come back -- as to when, who knows. But with these dividends and their record profits, I don't believe these sell-offs are warranted IMO.sounds like knife catching to me. As stated earlier in the thread - the comparitive attraction of the banks high yield diminishes as interest rates rise, and the banks are also facing various other risks at the moment. I've still got an open short position (partly closed the other day to cover the cost so the rest is free carried) - until it retraces I'll keep it open - there's no reason why it can't keep going down imo - so I'll stick with the trend for the time being until it retraces or volatility drops off.

But again, time will tell. For long term investors, "knife catching" is no real biggie, I've done it many times and eventually people will see how overdone this latest sell-off has been.

$1.13 fully franked dividend at $44.00 a stock? Are you for real? This is a great stock, CBA has been a proven performer for over a decade, and if any bank can ride out this turbulence, it's this one. I personally think this price is cheap, as are many banks, and am accumulating them because, eventually, they're going to come back -- as to when, who knows. But with these dividends and their record profits, I don't believe these sell-offs are warranted IMO.

But again, time will tell. For long term investors, "knife catching" is no real biggie, I've done it many times and eventually people will see how overdone this latest sell-off has been.

If you compared the 4 big banks.. I think CBA doesn't look as attractive as the others... and dont be fooled by the big dividends payment. Dividend can change at any time and with the subprime still yet to play out banks will be under plenty of down side for the next year or two.

read AFR "When banks feel the pain" over the weekend to see what lying ahead for them.

- Joined

- 8 November 2007

- Posts

- 314

- Reactions

- 0

CBA has always in the past performed very well, and I don't see what has fundamentally changed for people to dump this stock in favour for another bank? What does any other big 4 bank have to offer that CBA doesn't?If you compared the 4 big banks.. I think CBA doesn't look as attractive as the others... and dont be fooled by the big dividends payment. Dividend can change at any time and with the subprime still yet to play out banks will be under plenty of down side for the next year or two.

read AFR "When banks feel the pain" over the weekend to see what lying ahead for them.

ANZ: $22.50 @ 74c p/share = 3.29%

NAB: $29.50 @ 95c p/share = 3.22%

WBC: $22.50 @ 68c p/share = 3.02%

CBA: $44.00 @ 149c p/share = 3.39%

*NB: using Final Dividend prices to compare fairly

They're all roughly the same, so I don't understand people justifying comments like "doesn't look as attractive as the others". If any of the banks will withstand the storm, why would CBA be any worse off than any other of the banks? No-one has explained that.

- Joined

- 31 May 2006

- Posts

- 1,941

- Reactions

- 2

The banks were very good value in the early 90's when they were yielding 8%+ fully franked while interest rates were down around 6%. Westpac was under $3 from memory when Packer bought into it. I have vague recollections of NAB yielding 11% but that must have been a grossed up yield surely.

$1.13 fully franked dividend at $44.00 a stock? Are you for real? This is a great stock, CBA has been a proven performer for over a decade, and if any bank can ride out this turbulence, it's this one. I personally think this price is cheap, as are many banks, and am accumulating them because, eventually, they're going to come back -- as to when, who knows. But with these dividends and their record profits, I don't believe these sell-offs are warranted IMO.

But again, time will tell. For long term investors, "knife catching" is no real biggie, I've done it many times and eventually people will see how overdone this latest sell-off has been.

Other than the dividend and the current price, do you have any reason to think this is a great stock? The news out of ANZ today is just the beginning in what will be a steady stream of rising credit quality problems. It will start out as a trickle but gain momentum and will last at least for the next 12 months.

This is just the normal course of events as we move into the worst part of the credit cycle. However, given that the biggest credit bubble in history is imploding , this credit cycle could turn out to be anything but normal.

There are plenty of companies out there with growing earnings, that have attractive dividend yields that are not facing the headwinds that the banks will be facing in the medium term.

- Joined

- 8 November 2007

- Posts

- 314

- Reactions

- 0

For a long term investment, why would you knock it back? Yielding these dividends, I'm happy to hold no worries.Other than the dividend and the current price, do you have any reason to think this is a great stock? The news out of ANZ today is just the beginning in what will be a steady stream of rising credit quality problems. It will start out as a trickle but gain momentum and will last at least for the next 12 months.

This is just the normal course of events as we move into the worst part of the credit cycle. However, given that the biggest credit bubble in history is imploding , this credit cycle could turn out to be anything but normal.

There are plenty of companies out there with growing earnings, that have attractive dividend yields that are not facing the headwinds that the banks will be facing in the medium term.

As they say, buy when there's blood in the streets

") I'm sure many of you know how to make money, probably more so than me, but I invest only when everyone else is running away.

I'm sure many of you know how to make money, probably more so than me, but I invest only when everyone else is running away.Like everything in the market, eventually everyone starts to see the reality, and right now, it's all blurry and everyone is scared of the banks. Sounds like a good time to invest for the long term. I hope more people sell it down, only makes it cheaper for me to buy in and ride out this storm. Again, only my

, I've invested in worse times.- Joined

- 16 February 2008

- Posts

- 2,906

- Reactions

- 2

Sounds like there are a few Buffett lemmings around, without actually analysing "his techniques" and applying them.

Good luck to all though!

Just be VERY VERY careful at this moment! I think a LOT of fingers are going to get burnt before we see the end of this! Some absolutely HUGE moves following profit downgrades have occured so far and these profit downgrades may well ripple into the near future.

Many prices have been derived from the potential for big earnings growth, which does not appear to be happening. I have actually been shocked by the extent by which this slowdown seems to have actually hit the ASX companies, which will now be reflected in the rest of the indicators in the coming months, which may well cause another downturn in the market. The stockmarket is a "leading" indicator afterall, no?

Good luck to all though!

Just be VERY VERY careful at this moment! I think a LOT of fingers are going to get burnt before we see the end of this! Some absolutely HUGE moves following profit downgrades have occured so far and these profit downgrades may well ripple into the near future.

Many prices have been derived from the potential for big earnings growth, which does not appear to be happening. I have actually been shocked by the extent by which this slowdown seems to have actually hit the ASX companies, which will now be reflected in the rest of the indicators in the coming months, which may well cause another downturn in the market. The stockmarket is a "leading" indicator afterall, no?

- Joined

- 16 June 2005

- Posts

- 4,281

- Reactions

- 6

I was just looking at the course of sales for CBA today and noticed this:

07:05:43 AM 23.000 5,000 115,000.00 C

I assume there is a simple answer, but why did this sale occur @$23?

Thanks for the reply.

I believe CBA went ex-div today and most in-the-money call options (i.e.the strikes below where CBA closed yesterday = day before ex-div) would have been exercised. These usually show up around 7am the next morning. It it is possible the "C" at then end could mean "calls". Obviously someone owned some $23 calls and they have cashed in to get the dividend.

Over the next couple of days, it is quite likely to see a large number of in-the-money puts (i.e. put option strikes trading above CBA's price) being exercised and these will show up again around 7am.

Hope this helps!

- Joined

- 19 November 2007

- Posts

- 551

- Reactions

- 0

The ANZ is in trouble with Credit Default Swaps an OTC derivative which according to the Bank of International Settlements (BIS) is a major component of the more than $500 TRILLION of unregulated, non-clearing house guaranteed, private contracts and therefore without a market, pile of toxic OTC derivatives. So far the first part of the pile the CDOs and sub-prime derivatives have hit the fan, looks like the second much larger pile might be starting to shake.The news out of ANZ today is just the beginning in what will be a steady stream of rising credit quality problems. It will start out as a trickle but gain momentum and will last at least for the next 12 months.

This is just the normal course of events as we move into the worst part of the credit cycle. However, given that the biggest credit bubble in history is imploding , this credit cycle could turn out to be anything but normal.

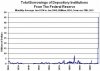

Sorry to post scary stuff, I know most people with bank shares are conservative risk averse people. However, if we really are in melt down mode the financial sector is where the nuclear reaction is epicentred.

The chart below shows the behind the scenes borrowing going on right now in the financial sector. Compare it to 1929, 1974, 1987, 2000, 9/11, etc...

Attachments

So_Cynical

The Contrarian Averager

- Joined

- 31 August 2007

- Posts

- 7,467

- Reactions

- 1,469

Thats a hell of a chart...real OMG stuff...even adjusted for inflation its a worse situation than the 1920's crash.

CBA has always in the past performed very well, and I don't see what has fundamentally changed for people to dump this stock in favour for another bank? What does any other big 4 bank have to offer that CBA doesn't?

ANZ: $22.50 @ 74c p/share = 3.29%

NAB: $29.50 @ 95c p/share = 3.22%

WBC: $22.50 @ 68c p/share = 3.02%

CBA: $44.00 @ 149c p/share = 3.39%

*NB: using Final Dividend prices to compare fairly

They're all roughly the same, so I don't understand people justifying comments like "doesn't look as attractive as the others". If any of the banks will withstand the storm, why would CBA be any worse off than any other of the banks? No-one has explained that.

Basing on dividend along doest justify...here is my quick reason why say WBC is better than CBA. For a start they employ better equity than CBA, they are also a smaller player but big enough to compete with CBA but small enough so if there is a defection in customers based WDC will get hit less than CBA.

smaller player has more room to grow than the bigger one.

Look at JB Hi-Fi and people like WOW and Harvey Norman and you can see small player if they have a good business model they have much better growth prospect.

WBC ROE

15.3 16.1 19.0 19.1 18.8 15.1 16.5 19.3 21.6 21.7

CBA ROE

18.6 17.7 10.0 13.5 14.3 10.2 11.7 16.4 18.2 18.4

PS I dont own any banking stock at this time in my portfolio because I think they all over price and too much of a market darling. so I patiently wait till the day I think it's justify their price and I buy. Even at these price I haven't even thinking about getting them just yet.

- Joined

- 4 February 2006

- Posts

- 564

- Reactions

- 0

PS I dont own any banking stock at this time in my portfolio because I think they all over price and too much of a market darling. so I patiently wait till the day I think it's justify their price and I buy. Even at these price I haven't even thinking about getting them just yet.

pretty much agree roe, major correction on financials underway and best the bulls will see this year is an exhaustion rally as its getting into some serious oversold territory

Haven't seen a major index or bluey recover fully in quicktime from a correction such as this - one hel l of a head of steam southbound atm

Attachments

Similar threads

- Replies

- 22

- Views

- 2K

- Replies

- 1

- Views

- 1K