skc

Goldmember

- Joined

- 12 August 2008

- Posts

- 8,277

- Reactions

- 329

Re: ACR - Acrux

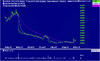

The release date for the FDA committee report was well flagged (see several posts above) so people exiting and not wanting to hold over this event is fully understandable. I think this is one of those examples where you can approach things with TA or FA and arrive the the same place.

Why don't you short it on the break of $1.50? Or do you not usually trade on the short side?

Given the chart patterns of recent weeks, with diverging momentum persisting for the last four, nobody can tell me that there haven't been some whispers on private lines suggesting "get out because..."

Level playing field, my tired foot

In any case: My $1.50 alert went off and went by without me buying because the second gradient did not hold as support. No further explanation needed why I don't set automatic conditional orders, but always reserve manual control.

The release date for the FDA committee report was well flagged (see several posts above) so people exiting and not wanting to hold over this event is fully understandable. I think this is one of those examples where you can approach things with TA or FA and arrive the the same place.

Why don't you short it on the break of $1.50? Or do you not usually trade on the short side?