Hi guys,

Despite being a CompSci grad with plenty of programming experience in the real world I have never looked at the many platforms people seem to use here for EAs and similar.

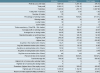

However, some back of envelope calculations (and I stress, back of envelope) give a high statistical probability of low risk/decent gains for this idea I had.

Place a short on spot gold at the end of NYMEX trading with stoploss at the NYMEX high.

Exit at the end of the Sydney trading session.

Would like to see how it turns out.

I am guessing this would not be too hard to code, anyone willing to give it a shot with some quick backtests?

Despite being a CompSci grad with plenty of programming experience in the real world I have never looked at the many platforms people seem to use here for EAs and similar.

However, some back of envelope calculations (and I stress, back of envelope) give a high statistical probability of low risk/decent gains for this idea I had.

Place a short on spot gold at the end of NYMEX trading with stoploss at the NYMEX high.

Exit at the end of the Sydney trading session.

Would like to see how it turns out.

I am guessing this would not be too hard to code, anyone willing to give it a shot with some quick backtests?