- Joined

- 26 May 2011

- Posts

- 120

- Reactions

- 0

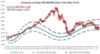

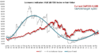

I've updated my ASX proxy analysis and thought I'd start a thread on the topic.

I love this sort of analysis, so perhaps it is useful for others too and hence the reason for my sharing.

Essentially it is a composite value analysis of the companies that make up the ASX20. Given the respective market cap of each company within, I think that it provides a good proxy for the XJO index. I may be able to extend it as far as the full XJO in the future, however 20 or so companies seems to be close enough to a limit for now. There are some issues such as debt levels, as there are a number of banks included. The valuations are a modification of the formula used by Roger Montgomery.

I don't use this information to trade on, however I find it very useful in putting the market in perspective and to help inform other investment decisions.

I'm happy to have feedback if there are any good suggestions for improvement. If there is sufficient interest, it is my intention to provide semi regular updates (monthly or quarterly).

I've attached the PDF View attachment XJO (ASX20 PROXY) AGGREGATE VALUE COMPOSITE INDEX.pdf

I'll be posting updates at http://macrovalueinvestment.blogspot.com/

I love this sort of analysis, so perhaps it is useful for others too and hence the reason for my sharing.

Essentially it is a composite value analysis of the companies that make up the ASX20. Given the respective market cap of each company within, I think that it provides a good proxy for the XJO index. I may be able to extend it as far as the full XJO in the future, however 20 or so companies seems to be close enough to a limit for now. There are some issues such as debt levels, as there are a number of banks included. The valuations are a modification of the formula used by Roger Montgomery.

I don't use this information to trade on, however I find it very useful in putting the market in perspective and to help inform other investment decisions.

I'm happy to have feedback if there are any good suggestions for improvement. If there is sufficient interest, it is my intention to provide semi regular updates (monthly or quarterly).

I've attached the PDF View attachment XJO (ASX20 PROXY) AGGREGATE VALUE COMPOSITE INDEX.pdf

I'll be posting updates at http://macrovalueinvestment.blogspot.com/

")

is that earnings momentum is best traded by price at least for individual companies – too much lag in information release unless you are truly expert in an industry/company.

is that earnings momentum is best traded by price at least for individual companies – too much lag in information release unless you are truly expert in an industry/company.